Brown v. Stored Value Cards, OR, Complaint, Debit Release Cards, 2015

Download original document:

Document text

Document text

This text is machine-read, and may contain errors. Check the original document to verify accuracy.

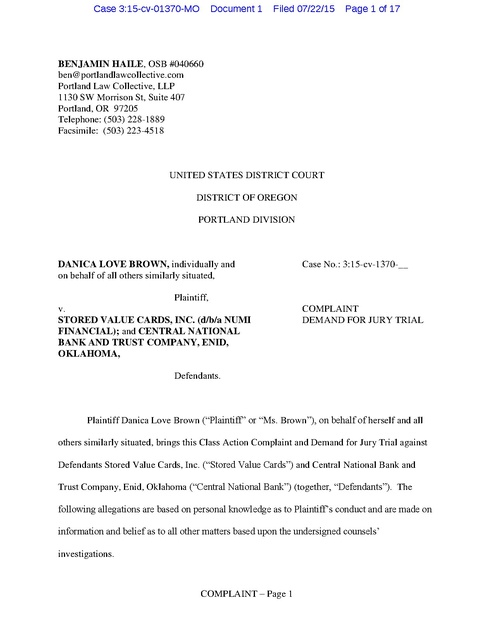

Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 1 of 17 BENJAMIN HAILE, OSB #040660 ben@portlandlawcollective.com Portland Law Collective, LLP 1130 SW Morrison St, Suite 407 Portland, OR 97205 Telephone: (503) 228-1889 Facsimile: (503) 223-4518 UNITED STATES DISTRICT COURT DISTRICT OF OREGON PORTLAND DIVISION DANICA LOVE BROWN, individually and on behalf of all others similarly situated, Plaintiff, v. STORED VALUE CARDS, INC. (d/b/a NUMI FINANCIAL); and CENTRAL NATIONAL BANK AND TRUST COMPANY, ENID, OKLAHOMA, Case No.: 3:15-cv-1370-__ COMPLAINT DEMAND FOR JURY TRIAL Defendants. Plaintiff Danica Love Brown (“Plaintiff” or “Ms. Brown”), on behalf of herself and all others similarly situated, brings this Class Action Complaint and Demand for Jury Trial against Defendants Stored Value Cards, Inc. (“Stored Value Cards”) and Central National Bank and Trust Company, Enid, Oklahoma (“Central National Bank”) (together, “Defendants”). The following allegations are based on personal knowledge as to Plaintiff’s conduct and are made on information and belief as to all other matters based upon the undersigned counsels’ investigations. COMPLAINT – Page 1 Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 2 of 17 INTRODUCTION 1. Plaintiff Danica Love Brown was arrested by Portland Police in November, 2014, during a peaceful protest of a Missouri grand jury’s decision not to charge Officer Darren Wilson in the shooting death of Michael Brown. Ms. Brown was charged with interfering with a peace officer and second-degree disorderly conduct. She was jailed for 8 hours at the Multnomah County Jail. Multnomah County Jail confiscated approximately $30 in cash from Ms. Brown when they booked her. When they released her 8 hours later they did not give her back her cash. Instead, Multnomah County Jail gave her a prepaid debit card. The card was issued by Defendants Stored Value Cards and Central National Bank and bore the insignia “NUMI Card.” 2. Ms. Brown would rather have received back her cash, but Multnomah County Jail forced the prepaid card upon her without presenting any alternatives to her. That prepaid card required Ms. Brown to pay fees to Defendants in order to access her own money. 3. Ms. Brown’s experience is illustrative of the experience of thousands of other individuals who have received NUMI Cards across the country. 4. Ms. Brown represented a captive consumer for Defendants and Defendants took full advantage of Ms. Brown’s complete lack of bargaining power by requiring Ms. Brown to pay various exorbitant, unreasonable fees to retrieve her money. Of course, Ms. Brown would never have agreed to receive her money in the form of the extremely expensive NUMI Card if she had been given any choice or bargaining power. 5. But, like the thousands of other pretrial detainees and former inmates that Defendants charge to spend their own money, Ms. Brown had no choice or bargaining power. Ms. Brown and the putative Class represent an involuntary market where consumers have no choice or say in whether they have to use prepaid debit cards to access their own money. COMPLAINT – Page 2 Case 3:15-cv-01370-MO 6. Document 1 Filed 07/22/15 Page 3 of 17 Defendants have engaged in a pattern of unlawful, deceptive, unfair and unconscionable profiteering and self-dealing with respect to the release cards that they forced upon individuals who are released from jails and prisons. In so doing, Defendants have also violated the Electronic Funds Transfer Act, 15 U.S.C. § 1693 et. seq. (“EFTA”). 7. As such, Ms. Brown files this class action lawsuit to redress injuries that she and a nationwide class of individuals have suffered and continue to suffer as a result of Defendants’ practices of forcing release cards upon pretrial detainees and former inmates that carry unreasonable and excessive fees that most consumers would never agree to if given a choice. THE PARTIES 8. Plaintiff Danica Love Brown lives in and is a citizen of Portland, Oregon. 9. Defendant Stored Value Cards, Inc. is a California corporation that does business under various trade names, including “Futura Card Services” and “NUMI Financial.” 10. Defendant Central National Bank & Trust Company, Enid, Oklahoma is an Oklahoma- based national bank with approximately $600 million in assets. Central National Bank has contracted with Stored Value Cards to issue prepaid debit cards to inmates being released from prisons and jails nationwide. JURISDICTION and VENUE 11. This Court has jurisdiction over the subject matter of this action pursuant to 28 U.S.C. § 1332(d) insofar as the amount in controversy exceeds $5 million and the Class is comprised of at least some persons who are citizens of states different from Defendants. 12. This Court also has jurisdiction over the subject matter of this action because this is a civil action arising under the laws of the United States, namely, the Electronic Funds Transfer COMPLAINT – Page 3 Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 4 of 17 Act, 15 U.S.C. § 1693 et. seq. This Court may exercise supplemental jurisdiction over state law claims pursuant to 28 U.S.C. § 1367. 13. Venue is proper in this District pursuant to 28 U.S.C. § 1391 because each Defendant is subject to personal jurisdiction in this District and a substantial part of the events or omissions giving rise to the claim occurred within this District. 14. Pursuant to § 646.638(2) of the Oregon Unfair Trade Practices Act, Plaintiff has mailed a copy of this Complaint to Attorney General Ellen F. Rosenblum at the Oregon Department of Justice, and attaches hereto as Exhibit A an affidavit to that effect. FACTS 15. Over 650,000 prisoners are released from state and federal prisons annually. Local jails nationwide process an estimated 11.6 million people each year. The vast majority of these individuals are released from custody shortly after they are booked. Most of the people released from jails are never convicted of any crime. 16. Traditionally, when individuals were released from jails, prisons, and other detention facilities, their jailers returned to them in the form of cash or check any cash that the jailers confiscated at booking. The jailers also traditionally returned to them in the form of cash or check any monies that had accrued in the individual’s prisoner trust account. 17. In many jurisdictions now, however, instead of receiving their account balances in cash or check upon release, prisoners are automatically given their account balances in the form of prepaid debit cards, or prison release cards. According to a recent Association of State Correctional Administrators survey, government agencies across the United States that handle prisoner funds are increasingly using prepaid debit cards to return personal funds to former prisoners. A majority of these agencies reported that a fee is charged when using the debit card COMPLAINT – Page 4 Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 5 of 17 to get cash from a bank. Several of the agencies indicated that they have been using some sort of release debit card for more than five years.1 18. Defendants market and distribute prepaid cards to jails and prisons around the country. 19. Stored Value Cards contracts with third party commissary companies and jail management software providers, who, in turn, contract with detention facilities to provide prepaid card programs to various city, county, and state agencies. 20. Stored Value Cards also contracts with Central National Bank as an issuing bank for its cards, and MasterCard as the payment network sponsor. 21. According to the NUMI Financial website, Defendants promise to “allow[] facilities to go completely cashless” and enable jails and prisons to “[e]liminate cash and checks.” 22. The card is activated and ready for immediate use when the consumer receives it. Consumers who receive the card do not even assign their own PIN to the card. A jail administrator does that. 23. Multnomah County Jail began to distribute NUMI prison release cards in or about 2014, after the Multnomah County Sheriff’s Office signed a four-year contract with Securus Technologies, Inc. Under that contract with Securus, the Sheriff’s Office implemented the debit card system run by Stored Value Cards. 24. Defendants provide the debit card system at no cost to the County. 25. The County agreed to release individuals with as little as $0.01 with a NUMI Card. 1 See http://www.asca.net/system/assets/attachments/7555/Use%20of%20Debit%20Cardsformatted%2 0Sheet1.pdf?1412189576 (last visited July 14, 2015); see also http://www.asca.net/system/assets/attachments/7553/Use%20of%20Debit%20Card%20for%20In mate%20Release%20Funds%20Survey.pdf?1412189540 (last visited July 14, 2015). COMPLAINT – Page 5 Case 3:15-cv-01370-MO 26. Document 1 Filed 07/22/15 Page 6 of 17 Multnomah County Jail has over 1,300 beds and processes an estimated 30,000 people annually. 27. These release cards are extremely profitable for Defendants, who charge their unwitting and unwilling customers exorbitant fees to possess and/or use the cards. 28. Defendants charge some consumers a $5.95 “monthly” service charge, which actually occurs only 5 days after an individual receives the card, not after the consumer has kept a card balance for at least a month. 29. Defendants charge other consumers a $3.50 “weekly” service charge, which actually occurs only 2 days after an individual receives the card, not after the consumer has kept a card balance for at least a week. 30. Defendants also charge a $9.95 card balance refund/paper check fee, which occurs when the cardholder requests account closure. Therefore, should a consumer wish to not use the card and receive a check, instead, it will cost her $9.95 to do so. 31. Defendants also charge a a. $2.95 ATM withdrawal fee (which is in addition to any surcharges that the ATM operator may assess); b. $4.95 international ATM withdrawal fee (which is in addition to any surcharges that the ATM operator may assess); c. $4.95 bank cash advance fee; d. $1.00 ATM balance inquiry fees; e. $1.50 ATM international balance inquiry fee; f. $1.95 declined ATM transaction fee; g. $0.50 automated customer service inquiry fee (the first one is free); COMPLAINT – Page 6 Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 7 of 17 h. $3.95 live customer service inquiry fee (the first one is free); i. $3.00 paper statement fee; and a j. $0.95 denial of transaction fee. 32. Defendants can charge and collect these exorbitant fees because their exclusive contracts with state and local agencies shield them from competitive market forces. 33. Individuals who are released from Multnomah County Jail have no choice but to accept a NUMI Card in lieu of receiving the return of their own money in the form of cash or check. They do not voluntarily engage the company, enroll in the program or take any affirmative steps to form any contractual relationship with Stored Value Cards, Central National Bank, or MasterCard. Ms. Brown’s Experience 34. Ms. Brown resides in Portland. 35. Ms. Brown was an adjunct faculty member at Metropolitan State College in Denver, Colorado, and is a PhD student in the doctoral program in social work at Portland State University. Her area of research focuses on understanding how the worldview of indigenous peoples can contribute to the development of behavioral health interventions and programs for urban Native American youth. 36. Ms. Brown was arrested by Portland Police on or about November 25, 2014, at approximately 7:00 p.m. 37. At the time of her arrest, Ms. Brown, along with hundreds of others, was participating in a peaceful protest march through downtown Portland, after a Missouri grand jury declined to indict Officer Darren Wilson for the shooting death of Michael Brown. COMPLAINT – Page 7 Case 3:15-cv-01370-MO 38. Document 1 Filed 07/22/15 Page 8 of 17 Ms. Brown was charged with interfering with a peace officer and second-degree disorderly conduct. Those charges were ultimately dismissed by the prosecution. 39. Ms. Brown was booked at the Multnomah County Jail. 40. Ms. Brown was released at approximately 2:00 a.m. on November 26, 2014. 41. At the time of her arrest, Ms. Brown had approximately $30 in cash on her person. 42. Multnomah County Jail confiscated Ms. Brown’s cash when they booked her. 43. Although she was only in jail overnight, Multnomah County Jail did not give Ms. Brown back her cash when they released her. Instead, Multnomah County Jail gave Ms. Brown a preloaded NUMI Card, which Defendants issued. 44. Ms. Brown’s NUMI Card had a balance of $30.97, which represented the cash that Multnomah County Jail confiscated from her. 45. Ms. Brown was never asked whether she wished to receive her monies in cash or in the form of a preloaded debit card for which she would be assessed various exorbitant fees. Ms. Brown never assented to receiving the card instead of her cash and never assented to the terms to any contract with Defendants. Ms. Brown was not given any opportunity to reject the card. Indeed, Ms. Brown had no choice but to accept the card instead of her cash; Ms. Brown could not meaningfully object to receiving the preloaded debit card. Ms. Brown’s receipt of her cash in the form of the NUMI Card was completely and utterly involuntary. 46. Between November 26, 2014, and December 3, 2014, Ms. Brown used the Card to make five small purchases. COMPLAINT – Page 8 Case 3:15-cv-01370-MO 47. Document 1 Filed 07/22/15 Page 9 of 17 Although Ms. Brown had received the Card only 5 days earlier, Defendants charged her a $5.95 “monthly” fee on December 1, 2014.2 48. Defendants also charged Ms. Brown a $0.95 service charge on December 1, 2014. 49. As such, in order to spend the $30.97 that the jail confiscated, Ms. Brown had to pay $6.90, or 22 percent of the monies the jail took from her. 50. Had Ms. Brown chosen to not use the Card and to close her account and receive a check, Defendants would have charged her $9.95 to do so, or 32 percent of the monies the jail took from her. CLASS CLAIMS 51. Defendants have engaged in the same conduct with respect to many other individuals across the United States. 52. Ms. Brown brings this action on behalf of herself and all others similarly situated pursuant to Fed. R. Civ. P. 23(a), 23(b)(2) and 23(b)(3) on behalf of the following nationwide classes: a. All persons who, upon release from a jail, prison, or detention facility, were provided with a prepaid card issued by Stored Value Cards, Inc., or its affiliates, and Central National Bank and Trust Company, Enid, Oklahoma, or its affiliates, that contained the balance of funds that had been previously confiscated from the 2 The subcontractor agreement negotiated between Multnomah County and Stored Value Cards demonstrates that the County asked Stored Value Cards to change its practice of charging the monthly service fee from 5 calendar days after receipt of the card to 5 business days. Stored Value Cards agreed, but never implemented that change. Therefore, although Stored Value Card’s subcontractor agreement with Multnomah County establishes that the $5.95 monthly fee will occur five business days after the consumer receives the NUMI Card, in Ms. Brown’s case, she received the card the day before the start of the 2014 Thanksgiving holiday, and Stored Value Cards charged her the monthly fee two business days later. COMPLAINT – Page 9 Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 10 of 17 person at the time of booking and paid a card fee in conjunction with the use or maintenance of the card. (“Class 1”) b. All persons who, upon release from a jail, prison, or detention facility, were provided with a prepaid card issued by Stored Value Cards, Inc., or its affiliates, and Central National Bank and Trust Company, Enid, Oklahoma, or its affiliates, that contained the balance of funds that had been previously held in that person’s inmate trust account and paid a card fee in conjunction with the use or maintenance of the card. (“Class 2”) 53. Additionally, Plaintiff seeks to represent the following Oregon subclasses (“Oregon Subclasses”): a. All persons who, upon release from a jail, prison, or detention facility in Oregon, were provided with a prepaid card issued by Stored Value Cards, Inc., or its affiliates, and Central National Bank and Trust Company, Enid, Oklahoma, or its affiliates, that contained the balance of funds that had been previously confiscated from the person at the time of booking and paid a card fee in conjunction with the use or maintenance of the card. (“Oregon Subclass 1”) b. All persons who, upon release from a jail, prison, or detention facility in Oregon, were provided with a prepaid card issued by Stored Value Cards, Inc., or its affiliates, and Central National Bank and Trust Company, Enid, Oklahoma, or its affiliates, that contained the balance of funds that had been previously held in that person’s inmate trust account and paid a card fee in conjunction with the use or maintenance of the card. (“Oregon Subclass 2”) (Class 1, Class 2, and the Oregon Subclasses are referred to herein as the “Class.”) COMPLAINT – Page 10 Case 3:15-cv-01370-MO 54. Document 1 Filed 07/22/15 Page 11 of 17 Plaintiff reserves the right to modify or amend the definition of the proposed Class before the Court determines whether certification is appropriate and as the Court may otherwise allow. 55. The Class is so numerous that joinder of all members is impracticable. Due to the nature of the commerce involved, the members of the Class are geographically dispersed throughout the United States. While the exact number of Class members is in the sole possession, custody and control of Defendants, Plaintiff believes that there are well in excess of 100 members. 56. Common questions of law and fact exist as to all members of the Class and predominate over any questions solely affecting individual members of the Class. Questions of law and fact common to the Class include but are not limited to whether: a. The prison release cards that the Class received were unsolicited electronic transfer cards; b. Defendants structured their prepaid card program to maximize the number and amount of fees they collected from the Class; c. Whether Stored Value Cards and/or Central National Bank were unjustly enriched through their prepaid card policies and practices; d. Whether Stored Value Cards and/or Central National Bank converted money belonging to the Class through their prepaid card policies and practices; e. Whether Stored Value Cards and/or Central National Bank subjected the Class to standardized policies and practices that were unconscionable and/or amounted to unlawful trade practices; f. Whether and what form(s) of relief should be afforded to the Class; and g. Whether the Class has suffered damages as a result of Defendants’ actions, and, if so, the measure and amount of such damages. COMPLAINT – Page 11 Case 3:15-cv-01370-MO 57. Document 1 Filed 07/22/15 Page 12 of 17 Plaintiff’s claims are typical of the claims of the other members of the Class she seeks to represent. Defendants’ practices have targeted and affected all members of the Class in a similar manner, i.e., they have all sustained damages arising out of Defendants’ practices. 58. Plaintiff will fully and adequately protect the interests of all members of the Class. Plaintiff has retained counsel experienced in both complex class action and consumer fraud litigation. Plaintiff has no interests which are adverse to or in conflict with the interests of the other members of the Class. 59. A class action is superior to other available methods for the fair and efficient adjudication of this controversy since joinder of all class members is impracticable. The prosecution of separate actions by individual members of the Class would impose heavy burdens upon the courts, and would create a risk of inconsistent or varying adjudications of the questions of law and fact common to the Class. A class action, on the other hand, would achieve substantial economies of time, effort, and expense, and would assure uniformity of decision with respect to persons similarly situated without sacrificing procedural fairness or bringing about other undesirable results. 60. The interests of the members of the Class in individually controlling the prosecution of separate actions are theoretical rather than practical. The Class has a high degree of cohesion, and prosecution of the action through representatives would be unobjectionable. The damages suffered by the individual Class members may be relatively small. Therefore, the expense and burden of individual litigation make it virtually impossible for class members to redress the wrongs done to them. Plaintiff anticipates no difficulty in management of this action as a class action. COMPLAINT – Page 12 Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 13 of 17 AS AND FOR A FIRST CAUSE OF ACTION (Violation of the Electronic Funds Transfer Act, 15 U.S.C. § 1693 et seq.) 61. Plaintiff re-alleges and incorporates by reference all of the allegations of this Complaint with the same force and affect as if fully restated herein. 62. The primary objective of the EFTA is to protect consumer rights by providing a basic framework establishing the rights, liabilities, and responsibilities of participants in the electronic fund and remittance transfer systems. 63. Among its consumer protection provisions, the EFTA prohibits the unsolicited issuance to a consumer of an electronic fund transfer card that does not meet all of the EFTA’s unsolicited access device criteria. See 15 U.S.C. § 1693(i). 64. Stored Value Cards and/or Central National Bank are financial institutions as defined by 15 U.S.C. § 1693a(9) because they directly hold accounts belonging to consumers. 65. Stored Value Cards and/or Central National Bank violated 15 U.S.C. § 1693(i) by issuing to consumers unsolicited electronic transfer cards that do not meet all of the EFTA’s unsolicited access device criteria. 66. Stored Value Cards and/or Central National Bank’s violations of the EFTA have caused and continue to cause Plaintiff and the Class damages. COMPLAINT – Page 13 Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 14 of 17 AS AND FOR A SECOND CAUSE OF ACTION (Violation of the Oregon Unfair Trade Practices Act, Oregon Revised Statutes §§ 646.605 et seq., on behalf of the Oregon Subclasses) 67. Plaintiff re-alleges and incorporates by reference all of the allegations of this Complaint with the same force and affect as if fully restated herein. 68. Plaintiff and the Oregon Subclasses have suffered an ascertainable loss as a result of Defendants’ unlawful trade practices and/or unconscionable tactics. 69. Defendants’ unlawful trade practices and/or unconscionable tactics were willful. 70. Defendants’ unlawful trade practices have caused and continue to cause Plaintiff and the Oregon Subclasses actual damages. AS AND FOR A THIRD CAUSE OF ACTION (Conversion) 71. Plaintiff re-alleges and incorporates by reference all of the allegations of this Complaint with the same force and affect as if fully restated herein. 72. Under Oregon law, “[c]onversion is an intentional exercise of dominion or control over chattel which so seriously interferes with the right of another to control it that the actor may justly be required to pay the other the full value of the chattel.” In re Complaint as to the Conduct of Martin, 328 Ore. 177, 184 (1998). 73. Defendants have wrongfully collected card fees from Plaintiff and members of the Class, and have taken specific and readily identifiable funds from Plaintiff and the members of the Class in payment of these fees in order to satisfy them. COMPLAINT – Page 14 Case 3:15-cv-01370-MO 74. Document 1 Filed 07/22/15 Page 15 of 17 Defendants, without proper authorization, assumed and exercised the right of ownership over these funds, in hostility to the rights of Plaintiff and the Class, without legal justification. 75. Defendants continue to retain these funds unlawfully and without the consent of Plaintiff or the Class. 76. Defendants intend to permanently deprive Plaintiff and the Class of these funds. 77. These funds are properly owned by Plaintiff and the Class, not Stored Value Cards or Central National Bank, which now claim that they are entitled to their ownership, contrary to the rights of Plaintiff and the Class. 78. Plaintiff and the Class are entitled to the immediate possession of these funds. 79. Defendants have wrongfully converted these specific and readily identifiable funds. 80. Stored Value Cards’ and Central National Bank’s wrongful conduct is continuing. 81. As a direct and proximate result of Defendants’ wrongful conversion, Plaintiff and the Class have suffered and continue to suffer damages. AS AND FOR A FOURTH CAUSE OF ACTION (Unjust Enrichment) 82. Plaintiff re-alleges and incorporates by reference all of the allegations of this Complaint with the same force and affect as if fully restated herein. 83. Defendants have been unjustly enriched by their assessment of fees upon Plaintiff and the Class that are unfair, unconscionable, inflated and oppressive. 84. The circumstances are such that it would be unjust and inequitable for Defendants to retain the benefit that they unjustly received from Plaintiff and the Class. 85. Plaintiff and the Class have suffered and continue to suffer actual damages as a result of Defendants’ unjust retention of proceeds from their acts and practices alleged herein. COMPLAINT – Page 15 Case 3:15-cv-01370-MO Document 1 Filed 07/22/15 Page 16 of 17 DEMAND FOR JURY TRIAL Plaintiff respectfully requests jury trial of all claims that can be so tried. PRAYER FOR RELIEF WHEREFORE, Plaintiff, on behalf of herself and on behalf of the Class, prays for the following relief: 1. An order certifying this case as a class action and appointing Plaintiff and the undersigned counsel to represent the Class; 2. Declaration, judgment, and decree that Defendants Stored Value Cards’ and/or Central National Bank’s conduct alleged herein: 3. a. Violates the EFTA; b. Constitutes conversion; and c. Constitutes unjust enrichment; Declaration, judgment, and decree that Defendants Stored Value Cards’ and/or Central National Bank’s conduct alleged herein violates the OUTPA; 4. Damages to Plaintiff and the Class to the maximum extent allowed under state and federal law; 5. Costs and disbursements of the action; 6. Restitution and/or disgorgement of ill-gotten gains; 7. Pre- and post-judgment interest; 8. Reasonable attorneys’ fees; 9. An injunction requiring corrective measures to be taken to prevent Defendants from engaging in the above-described misconduct; and COMPLAINT – Page 16 Case 3:15-cv-01370-MO 10. Document 1 Filed 07/22/15 Page 17 of 17 Such other relief, in law and equity, as this Court may deem just and proper. DATED this 22nd day of July, 2015. THE PORTLAND LAW COLLECTIVE, LLP ________________________ Benjamin Haile 1130 SW Morrison Street, Suite 407 Portland, OR 97205 THE HUMAN RIGHTS DEFENSE CENTER Lance Weber (To Be Admitted Pro Hac Vice) Sabarish Neelakanta (To Be Admitted Pro Hac Vice) PO Box 1151 Lake Worth, FL 33460 GISKAN SOLOTAROFF ANDERSON & STEWART LLP Raymond Audain (To Be Admitted Pro Hac Vice) Oren Giskan (To Be Admitted Pro Hac Vice) 11 Broadway - Suite 2150 New York, NY 10004 ATTORNEYS FOR PLAINTIFF AND THE CLASS COMPLAINT – Page 17