Gao Report to Us House Subcommittee on Gov Reform Re Bureau of Prisons Contract Payments 2002

Download original document:

Document text

Document text

This text is machine-read, and may contain errors. Check the original document to verify accuracy.

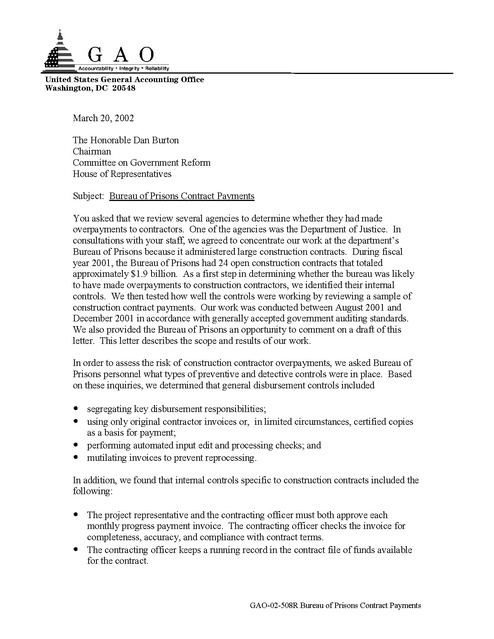

United States General Accounting Office Washington, DC 20548 March 20, 2002 The Honorable Dan Burton Chairman Committee on Government Reform House of Representatives Subject: Bureau of Prisons Contract Payments You asked that we review several agencies to determine whether they had made overpayments to contractors. One of the agencies was the Department of Justice. In consultations with your staff, we agreed to concentrate our work at the department’s Bureau of Prisons because it administered large construction contracts. During fiscal year 2001, the Bureau of Prisons had 24 open construction contracts that totaled approximately $1.9 billion. As a first step in determining whether the bureau was likely to have made overpayments to construction contractors, we identified their internal controls. We then tested how well the controls were working by reviewing a sample of construction contract payments. Our work was conducted between August 2001 and December 2001 in accordance with generally accepted government auditing standards. We also provided the Bureau of Prisons an opportunity to comment on a draft of this letter. This letter describes the scope and results of our work. In order to assess the risk of construction contractor overpayments, we asked Bureau of Prisons personnel what types of preventive and detective controls were in place. Based on these inquiries, we determined that general disbursement controls included • segregating key disbursement responsibilities; • using only original contractor invoices or, in limited circumstances, certified copies as a basis for payment; • performing automated input edit and processing checks; and • mutilating invoices to prevent reprocessing. In addition, we found that internal controls specific to construction contracts included the following: • The project representative and the contracting officer must both approve each monthly progress payment invoice. The contracting officer checks the invoice for completeness, accuracy, and compliance with contract terms. • The contracting officer keeps a running record in the contract file of funds available for the contract. GAO-02-508R Bureau of Prisons Contract Payments • Final contract payment is not made until all required work is verified as complete and all open claims have been satisfied. We reviewed a sample of 27 payments on five different construction contracts to assess whether the construction contract payment controls were properly designed and whether they were in place and operating to prevent or detect overpayments for the selected items.1 The contracts totaled approximately $186 million. The 27 payments selected for review totaled approximately $31 million, including the final payment for each of the five construction contracts. For each payment selected, we reviewed the payment file and obtained clarifications from Bureau of Prisons personnel when necessary. For the payments that we reviewed, we found that the internal controls were in place and operating and that construction contract payment amounts were correct, or, that if errors occurred, they were detected and corrected promptly as a normal part of the payment system. We found a few minor clerical errors for three of the contracts we reviewed. The errors were subsequently detected and corrected by the Bureau of Prisons through its own routine detective control procedures before we made our review. For example, in one contract, there was an overpayment of $3 on a payment of about $4 million. The error was rectified the following month by reducing the next month’s payment by $3. In a second contract, the increase in retainage (costs to be paid later in the contract) was $11,581 more than the contract costs incurred during the same period. In the following payment period, this error was corrected by reducing the retainage payment by $11,581. The risk of undetected construction contractor overpayments at the Bureau of Prisons does not appear to be significant based on the controls in place and operating at the time we made our tests. Because of this, and as agreed with your staff, we believe no further work relative to this request is warranted at this time. In an oral response to a draft of this letter, the bureau stated that it had no comments. We are sending copies of this letter to the ranking minority member of the House Committee on Government Reform and the Bureau of Prisons. Copies of this letter are available to other interested parties. This letter will also be available on GAO’s home page at http://www.gao.gov. 1 These contracts were selected because they had been closed in fiscal year 2001, allowing us to review the full activity of the contracts. They included three construction contracts for two prisons and two related contracts for monitoring and oversight. Because our sample was not statistically based, our conclusions are drawn solely for the transactions we reviewed and cannot be extrapolated to all construction contract payments. 2 GAO-02-508R Bureau of Prisons Contract Payments If you have any questions, please contact me at (202) 512-9508 or by e-mail at Calboml@gao.gov or my Assistant Director, Mark P. Connelly, at (202) 512-8795 or by e-mail at Connellym@gao.gov. Key contributors to this letter were Don Campbell and Jack Warner. Sincerely yours, Linda Calbom Director, Financial Management and Assurance (190028) 3 GAO-02-508R Bureau of Prisons Contract Payments