Iowa Dept Human Services Five Year Audit 2005 Thru 2011

Download original document:

Document text

Document text

This text is machine-read, and may contain errors. Check the original document to verify accuracy.

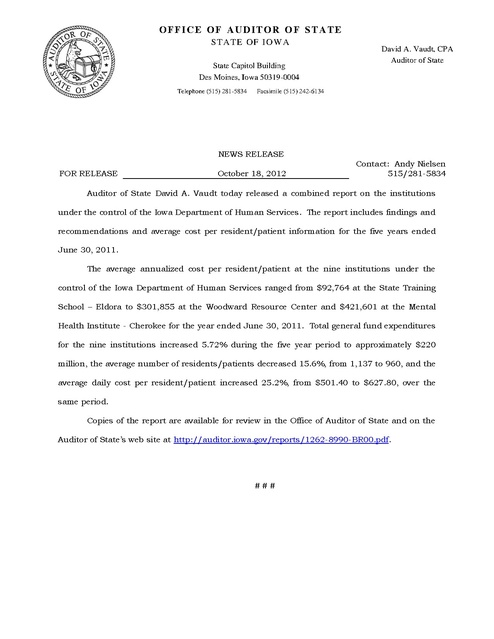

OFFICE OF AUDITOR OF STATE ST AT E OF IOWA State Capitol Building Des Moines, Iowa 50319-0004 Telephone (515) 281-5834 David A. Vaudt, CPA Auditor of State Facsimile (515) 242-6134 NEWS RELEASE FOR RELEASE October 18, 2012 Contact: Andy Nielsen 515/281-5834 Auditor of State David A. Vaudt today released a combined report on the institutions under the control of the Iowa Department of Human Services. The report includes findings and recommendations and average cost per resident/patient information for the five years ended June 30, 2011. The average annualized cost per resident/patient at the nine institutions under the control of the Iowa Department of Human Services ranged from $92,764 at the State Training School – Eldora to $301,855 at the Woodward Resource Center and $421,601 at the Mental Health Institute - Cherokee for the year ended June 30, 2011. Total general fund expenditures for the nine institutions increased 5.72% during the five year period to approximately $220 million, the average number of residents/patients decreased 15.6%, from 1,137 to 960, and the average daily cost per resident/patient increased 25.2%, from $501.40 to $627.80, over the same period. Copies of the report are available for review in the Office of Auditor of State and on the Auditor of State’s web site at http://auditor.iowa.gov/reports/1262-8990-BR00.pdf. ### COMBINED REPORT ON THE INSTITUTIONS UNDER THE CONTROL OF THE IOWA DEPARTMENT OF HUMAN SERVICES SCHEDULES FINDINGS AND RECOMMENDATIONS JUNE 30, 2011 Office of AUDITOR OF STATE State Capitol Building Des Moines, Iowa David A. Vaudt, CPA Auditor of State Table of Contents Page Auditor of State’s Report 3 Overview 4-6 Schedules: Schedule Average Cost Per Resident/Patient Information by Institution Fiscal Years 2007 through 2011 Average Cost Per Resident/Patient Information – Graphs: Total Expenditures Average Number of Residents/Patients Average Annualized Cost per Resident/Patient General Fund Expenditures by Institution - 2007 General Fund Expenditures by Institution - 2008 General Fund Expenditures by Institution - 2009 General Fund Expenditures by Institution - 2010 General Fund Expenditures by Institution - 2011 Resident/Patient Population Statistics - 2011 1 8-11 2 3 4 5 6 7 13 14 15 16-17 18-19 20-21 22-23 24-25 26-27 Findings and Recommendations: Mental Health Institute - Clarinda Mental Health Institute - Mount Pleasant Mental Health Institute - Cherokee Mental Health Institute - Independence Woodward Resource Center Glenwood Resource Center State Juvenile Home - Toledo State Training School - Eldora Civil Commitment Unit for Sexual Offenders 1262-8990-BR00 28-29 30 31 32 33-34 35 36 37 38 OFFICE OF AUDITOR OF STATE ST AT E OF IOWA State Capitol Building Des Moines, Iowa 50319-0004 Telephone (515) 281-5834 David A. Vaudt, CPA Auditor of State Facsimile (515) 242-6134 October 9, 2012 To the Council Members of the Iowa Department of Human Services: The Institutions under the control of the Iowa Department of Human Services are a part of the State of Iowa and, as such, have been included in our audits of the State’s Comprehensive Annual Financial Report (CAFR) and the State’s Single Audit Report for the year ended June 30, 2011. In conducting our audits, we became aware of certain aspects concerning the various Institutions’ operations for which we believe corrective action is necessary. As a result, we have developed recommendations which are reported on the following pages. We believe you should be aware of these recommendations, which include recommendations pertaining to internal control and compliance with statutory requirements and other matters. These recommendations have been discussed with applicable Institution personnel and their responses to these recommendations are included in this report. While we have expressed our conclusions on the Institutions’ responses, we did not audit the Institutions’ responses and, accordingly, we express no opinion on them. We have also included certain unaudited financial and other information for the Institutions under the control of the Iowa Department of Human Services for the five years ended June 30, 2011 to report an average cost per resident/patient at each Institution as required by Chapter 11.28 of the Code of Iowa. This report, a public record by law, is intended solely for the information and use of the officials and employees of the Iowa Department of Human Services, the Institutions under the control of the Iowa Department of Human Services, citizens of the State of Iowa and other parties to whom the Iowa Department of Human Services may report. This report is not intended to be and should not be used by anyone other than these specified parties. We would like to acknowledge the many courtesies and assistance extended to us by personnel of the Institutions during the course of our audits. Should you have questions concerning any of the above matters, we shall be pleased to discuss them with you at your convenience. Individuals who participated in our audits of the Institutions are listed on pages 29, 30, 31, 32, 34, 35, 36, 37 and 38 and they are available to discuss these matters with you. DAVID A. VAUDT, CPA Auditor of State cc: WARREN G. JENKINS, CPA Chief Deputy Auditor of State Honorable Terry E. Branstad, Governor David Roederer, Director, Department of Management Glen P. Dickinson, Director, Legislative Services Agency 3 Iowa Department of Human Services Overview Background In accordance with Chapter 218 of the Code of Iowa, the Iowa Department of Human Services has the authority to control, manage, direct and operate the following institutions: Mental Health Institute - Clarinda – The Institute has been serving the citizens of Southwest Iowa since 1888. The function of this Institute is to promote good mental health practices and to provide high level care for persons with mental illness. Levels of care provided are adult in-patient psychiatric and gero-psychiatric. Mental Health Institute - Mount Pleasant – The Institute was established on February 2, 1861. Major goals and objectives of the Institute are to be responsive to the communityoriented patient care needs of the population it serves, without duplicating services already provided in the community. Levels of care provided are adult in-patient psychiatric and dual diagnosis. Mental Health Institute - Cherokee – The Institute was founded in 1902. The Institute is responsible for furnishing psychiatric services to citizens of Northwest Iowa counties to the extent such services are not provided by other sources. Levels of care provided are adult in-patient psychiatric and child and adolescent in-patient psychiatric. Mental Health Institute - Independence – The Institute was established on May 1, 1873. The Institute is a fully accredited psychiatric care hospital and provides treatment for mentally ill adults, adolescents and children. Levels of care provided are adult inpatient psychiatric, child and adolescent in-patient psychiatric and psychiatric-medical institute for children. Woodward Resource Center – The Resource Center was established in 1917. The Center is a residential facility for the mentally retarded and provides treatment, training, instruction, care, habilitation and support of persons with an intellectual disability or other disabilities in the State. Glenwood Resource Center – The Resource Center was established on September 1, 1876. The Center is a residential facility for the mentally retarded and provides treatment, training, instruction, care, habilitation and support of persons with an intellectual disability or other disabilities in the State. State Juvenile Home - Toledo – The Juvenile Home was established on October 21, 1920. This Institution is a structured, non-secure co-ed facility serving juveniles under 17 who are residents of the State of Iowa in need of assistance. The residents are committed by the juvenile courts as dependent or neglected or are committed voluntarily through application to the County Board of Supervisors and the Iowa Department of Human Services. The children become wards of the State to receive educational, medical, diagnostic treatment and limited employment programs to help them attain productive and satisfying citizenship in a free society. State Training School - Eldora – The Training School was established in 1868. The Institution is a minimum security facility for boys between the ages of twelve and eighteen who have been adjudicated delinquent by the juvenile courts of the State of Iowa. Effective January 1, 1992, a diagnosis and evaluation center and other units were established to provide juvenile delinquents a program which focuses upon appropriate developmental skills, treatment, placement and rehabilitation. 4 Iowa Department of Human Services Overview Civil Commitment Unit for Sexual Offenders (CCUSO) – The Civil Commitment Unit for Sexual Offenders was established in 1999. The Unit provides treatment for sexually violent predators in a secure facility located in Cherokee, Iowa. The residents have completed their criminal sentences, have been identified as a high risk for a repeat offense and are committed through a civil action by order of the courts. As mentioned on the previous page, different levels of care are provided at each of the Mental Health Institutes. They are: Adult In-patient Psychiatric – This program, licensed as a hospital, represents traditional, in-hospital psychiatric care for persons 18 years of age and older. It includes 24-hour nursing care and 24-hour medical and psychiatric on call coverage. Child and Adolescent In-patient Psychiatric – This program, licensed as a hospital, represents traditional, in-hospital psychiatric care for persons under 18 years of age. It includes a required educational component and 24-hour nursing care and 24-hour medical and psychiatric on-call coverage. Gero-Psychiatric – This program, licensed as nursing home care, represents 24-hour custodial care for persons declared disabled or over age 65. There is some level of 24hour nursing care and periodic medical and psychiatric care. Generally, these persons are beyond the capacity of community providers to care for. Psychiatric-Medical Institute for Children (PMIC) – This program, licensed as a PMIC, represents 24-hour care and behavior management for persons 12 to 17 years of age requiring intensive behavioral treatment modalities. There is periodic nursing and psychiatric coverage. Generally, these children are beyond the care of privately administered PMIC’s in the state. Dual Diagnosis – This program represents a 28-day residential substance dependence treatment program for persons with co-morbid mental illness. There is periodic nursing, medical and psychiatric coverage. It is the only program for this population in the state of Iowa. Scope and Methodology We have calculated an average cost per resident/patient at each Institution for the five years ended June 30, 2011 based on their general fund expenditures. Certain reclassifications and changes have been made to these expenditures to provide comparable averages between Institutions. Therefore, expenditure amounts and cost per resident/patient averages may differ from those used for statewide financial statement purposes. These reclassifications and changes are as follows: (1) Operating transfers, primarily reimbursements to other state agencies for services, have been reclassified as expenditures for purposes of this report. (2) At the inception of a capital lease, total principal payments are recorded as expenditures and as other financing sources for statewide purposes. For purposes of this report, we have included only the current year principal and interest payments as expenditures. (3) Canteen operations have been excluded from general fund expenditures since the canteen is a self-supporting operation at each Institution. (4) Non-cash assistance, consisting of USDA commodities, has been excluded from general fund expenditures. 5 Iowa Department of Human Services Overview Median stay information was not calculated or presented in the accompanying average cost per resident/patient schedule for the resource centers or juvenile facilities since the median stay tends to be for a much longer period. The average annualized cost per resident/patient is calculated using the average number of occupied resident beds. Since the median stay at the Mental Health Institutes tends to be less than the stay at the other Institutions, the cost per stay was calculated for each of the Mental Health Institutes. This represents the average cost for the median stay of each patient admitted. Summary Observation The Mental Health Institute – Cherokee provides significant outpatient services not performed by other Institutions. Adequate statistical data on outpatient services, including the amount and cost of services provided by year, was not readily available. Accordingly, the cost per resident/patient information at the Mental Health Institute - Cherokee is not comparable to other Institutions and may not be comparable between years at the Mental Health Institute - Cherokee. The amount of support services the Mental Health Institute – Cherokee provided for the Civil Commitment Unit for Sexual Offenders is reported as reallocated support services costs on Schedules 2, 3, 4, 5 and 6 on pages 16 through 25. The Woodward Resource Center and the Glenwood Resource Center also provide significant supported community living services, respite and supported employment services which are paid through Iowa Medicaid and Community Based Services (HCBS) Waivers. The cost of providing these services is included in the cost per resident calculation. However, the number of individuals served is not included in the average number of residents. The average annualized cost per resident/patient ranged from $92,764 at the State Training School – Eldora to $301,855 at the Woodward Resource Center and $421,601 at the Mental Health Institute – Cherokee for fiscal year 2011. Total general fund expenditures increased 5.72%, from $208,083,701 in 2007 to $219,981,354 in 2011, the average number of residents/patients decreased 15.6%, from 1,137 to 960, and the average daily cost per resident/patient increased 25.2%, from $501.40 to $627.80, over the same period. Median stay ranged from 9 days to 44 days at the four Mental Health Institutes for fiscal year 2011. 6 Iowa Department of Human Services 7 Institutions Under the Control of the Iowa Department of Human Services Average Cost Per Resident/Patient by Institution (Unaudited) For the Last Five Fiscal Years Year ended June Average Average Average Annualized Number of Number Cost per Residents/ of EmResident/ Patients ployees Patient Mental Health Institute - Clarinda 48 91 Mental Health Institute - Mt. Pleasant 59 Mental Health Institute - Cherokee Mental Health Institute - Independence Cost per Stay 176,892 484.64 21 $ 10,177 101 132,795 363.82 28 10,187 40 213 344,165 942.92 14 13,201 86 283 243,051 665.89 48 31,963 Woodward Resource Center 248 697 221,510 606.88 Glenwood Resource Center 338 920 217,387 595.58 State Juvenile Home - Toledo 79 118 104,366 285.93 State Training School - Eldora 173 197 79,748 218.49 66 78 100,552 275.49 1,137 2,698 183,011 501.40 Civil Commitment Unit for Sexual Offenders Total 8 $ 30, 2007 Average Daily Cost per Median Resident/ Stay Patient (Days) $ Schedule 1 Average Number of Residents/ Patients Year ended June Average Average Annualized Number Cost per of EmResident/ ployees Patient 46 93 60 $ 30, 2008 Average Daily Cost per Median Resident/ Stay Patient (Days) Cost per Stay Average Number of Residents/ Patients Year ended June 30, 2009 Average Average Average Annualized Daily Number Cost per Cost per Median of EmResident/ Resident/ Stay ployees Patient Patient (Days) 196,548 538.49 19 $ 10,231 44 92 106 144,064 394.70 28 11,052 66 40 212 362,275 992.53 13 12,903 84 280 259,768 711.69 36 25,621 235 717 247,023 326 927 76 209,599 574.24 8 $ 4,594 107 137,009 375.37 26 9,760 38 205 376,881 1,032.55 14 14,456 82 278 273,346 748.89 37 27,709 676.77 218 729 288,813 791.27 242,674 664.86 314 932 260,964 714.97 118 117,810 322.77 72 123 125,631 344.19 166 194 89,716 245.80 160 201 96,100 263.29 71 84 108,292 296.69 78 92 114,036 312.43 1,104 2,731 201,716 552.65 1,072 2,759 217,557 596.05 $ 9 $ Cost per Stay $ Institutions Under the Control of the Iowa Department of Human Services Average Cost Per Resident/Patient by Institution (Unaudited) For the Last Five Fiscal Years Average Number of Residents/ Patients Year ended June 30, 2010 Average Average Average Annualized Daily Number Cost per Cost per Median of EmResident/ Resident/ Stay ployees Patient Patient (Days) Mental Health Institute - Clarinda 47 85 Mental Health Institute - Mt. Pleasant 71 Mental Health Institute - Cherokee Mental Health Institute - Independence 182,805 500.83 9 97 120,963 331.41 28 9,279 34 194 387,690 1,062.17 15 15,932 78 262 274,225 751.30 48 36,062 Woodward Resource Center 205 724 318,359 872.22 Glenwood Resource Center 300 922 269,879 739.39 State Juvenile Home - Toledo 75 114 115,320 315.95 State Training School - Eldora 141 188 99,726 273.22 80 89 121,179 332.00 1,031 2,675 223,456 612.21 Civil Commitment Unit for Sexual Offenders Total 10 $ Cost per Stay $ $ 4,508 Schedule 1 Average Number of Residents/ Patients Year ended June 30, 2011 Average Average Average Annualized Daily Number Cost per Cost per Median of EmResident/ Resident/ Stay ployees Patient Patient (Days) 40 80 63 $ Cost per Stay 207,391 568.19 9 92 134,204 367.68 29 10,663 27 157 421,601 1,155.07 12 13,861 59 233 345,732 947.21 44 41,677 201 711 301,855 827.00 286 883 276,437 757.36 60 103 141,266 387.03 143 169 92,764 254.15 81 88 123,141 337.37 960 2,516 229,147 627.80 $ $ 5,114 11 Iowa Department of Human Services 12 Institutions Under the Control of the Iowa Department of Human Services Average Cost Per Resident by Institution Total Expenditures (Unaudited) For the Last Five Fiscal Years $ 60,000,000 55,000,000 50,000,000 Total Expenditures 45,000,000 o 2007 40,000,000 30,000,000 • 2008 • 2009 25,000,000 o 2010 20,000,000 • 35,000,000 2011 15,000,000 10,000,000 5,000,000 Clarinda Mt. Pleasant Cherokee Independence $ 90,000,000 Total Expenditures 80,000,000 70,000,000 60,000,000 o 2007 50,000,000 • 2008 • 2009 40,000,000 30,000,000 o 2010 20,000,000 • 10,000,000 Woodward Glenwood Toledo 13 Eldora CCUSO 2011 Institutions Under the Control of the Iowa Department of Human Services Average Cost Per Resident by Institution Average Number of Residents (Unaudited) For the Last Five Fiscal Years 500 400 2007 D 2008 350 2009 300 2010 250 2011 200 150 100 50 Clarinda Mt. Pleasant Cherokee Independence 500 Average Number of Residents Average Number of Residents 450 450 400 2007 350 2008 300 2009 2010 250 2011 200 150 100 50 - Woodward Glenwood Toledo 14 Eldora CCUSO Institutions Under the Control of the Iowa Department of Human Services Average Cost Per Resident by Institution Average Annual Cost per Resident (Unaudited) Average Annualized Cost per Resident For the Last Five Fiscal Years $ 450,000 420,000 390,000 360,000 330,000 300,000 270,000 240,000 210,000 180,000 150,000 120,000 90,000 60,000 30,000 - 2007 D 2008 2009 2010 2011 Clarinda Average Annualized Cost per Resident $ Mt. Pleasant Cherokee Independence 330,000 300,000 270,000 240,000 210,000 2007 180,000 2008 2009 150,000 2010 120,000 2011 90,000 60,000 30,000 Woodward Glenwood Toledo 15 Eldora CCUSO Institutions Under the Control of the Iowa Department of Human Services General Fund Expenditures by Institution (Unaudited) Year ended June 30, 2007 Pe rsonal se rvice s Me ntal He alth Me ntal He alth Me ntal He alth Me ntal He alth Woodward Institute - Institute - Institute - Institute - Re source Clarinda Mount Ple asant Che roke e Inde pe nde nce Ce nte r $ 6,974,408 6,607,924 13,097,593 17,987,635 32,341 21,055 61,512 47,868 163,525 Supplie s and mate rials 784,206 474,112 953,231 929,528 3,761,111 Contractual se rvice s 534,099 636,244 1,408,683 1,874,328 4,818,602 Capital outlay 164,335 93,516 164,310 55,466 1,895,961 Claims and misce llane ous 709 27 3,144 492 147,097 Lice nse s, pe rmits and re funds 732 - 154 7,082 870 - 2,016 - - - 8,490,830 7,834,894 15,688,627 20,902,399 54,934,382 Trave l Aid to individuals Total be fore re allocations $ Re allocate d support se rvice s costs (se e page 6) (1,922,019) Total $ 16 13,766,608 44,147,216 Schedule 2 State State Civil Gle nwood Juve nile Training Commitme nt Re source Home - School - Unit for Se xual Ce nte r Tole do Eldora Offe nde rs Total 55,176,264 6,787,256 11,267,363 4,502,835 235,937 20,081 69,613 34,646 166,548,494 686,578 5,649,422 598,421 706,984 27,255 13,884,270 8,331,823 736,550 1,439,726 129,846 19,909,901 3,583,845 94,876 301,082 19,305 6,372,696 497,445 5,135 8,167 549 662,765 2,186 2,572 3,385 - 16,981 - - - - 2,016 73,476,922 8,244,891 13,796,320 4,714,436 208,083,701 1,922,019 6,636,455 17 Institutions Under the Control of the Iowa Department of Human Services General Fund Expenditures by Institution (Unaudited) Year ended June 30, 2008 Pe rsonal se rvice s Me ntal He alth Me ntal He alth Me ntal He alth Me ntal He alth Woodward Institute - Institute - Institute - Institute - Re source Clarinda Mount Ple asant Che roke e Inde pe nde nce Ce nte r $ 7,391,770 7,216,650 13,682,846 18,417,624 40,638 33,797 43,114 58,315 495,664 Supplie s and mate rials 990,920 532,517 977,555 987,342 3,634,099 Contractual se rvice s 554,287 773,252 1,535,253 2,031,591 4,946,799 63,397 86,227 231,219 323,034 1,689,921 126 405 1,409 1,035 140,380 85 1,010 505 1,578 407 - - - - - 9,041,223 8,643,858 16,471,901 21,820,519 58,050,366 Trave l Capital outlay Claims and misce llane ous Lice nse s, pe rmits and re funds Aid to individuals Total be fore re allocations $ Re allocate d support se rvice s costs (se e page 6) (1,980,918) Total $ 18 14,490,983 47,143,096 Schedule 3 State State Civil Gle nwood Juve nile Training Commitme nt Re source Home - School - Unit for Se xual Ce nte r Tole do Eldora Offe nde rs Total 60,378,764 7,221,028 12,104,745 5,091,505 440,068 33,390 60,763 65,017 1,270,766 6,366,174 695,767 752,121 106,345 15,042,840 8,314,399 759,312 1,554,480 274,163 20,743,536 3,073,359 236,224 400,995 169,134 6,273,510 532,949 6,139 14,524 1,678 698,645 5,939 1,676 5,222 - 16,422 226 - - - 226 79,111,878 8,953,536 14,892,850 5,707,842 222,693,973 1,980,918 7,688,760 19 178,648,028 Institutions Under the Control of the Iowa Department of Human Services General Fund Expenditures by Institution (Unaudited) Year ended June 30, 2009 Me ntal He alth Me ntal He alth Me ntal He alth Me ntal He alth Pe rsonal se rvice s $ Woodward Institute - Institute - Institute - Institute - Re source Clarinda Mt. Ple asant Che roke e Inde pe nde nce Ce nte r 7,529,126 7,385,240 13,819,279 19,051,691 84,462 22,152 44,692 73,630 580,285 Supplie s and mate rials 897,809 580,518 1,222,413 965,007 4,149,086 Contractual se rvice s 591,079 979,587 950,191 2,077,976 6,129,541 Capital outlay 119,038 73,686 307,189 240,646 1,901,365 Claims and misce llane ous 359 840 331 3,149 147,139 Lice nse s, pe rmits and re funds 465 - 780 2,309 607 - 540 - - - 9,222,338 9,042,563 16,344,875 22,414,408 62,961,270 Trave l Aid to individuals Total $ Re allocate d support se rvice s costs (se e page 6) (2,023,410) Total $ 20 14,321,465 50,053,247 Schedule 4 State State Civil Gle nwood Juve nile Training Commitme nt Re source Home - School - Unit for Se xual Ce nte r Tole do Eldora Offe nde rs Total 62,500,842 7,651,720 12,287,820 5,827,528 254,567 17,633 55,147 7,240 1,139,808 6,584,419 677,889 855,556 786,475 16,719,172 9,289,745 659,861 1,849,605 195,958 22,723,543 2,785,072 29,723 307,860 53,657 5,818,236 520,882 4,332 18,818 569 696,419 7,116 4,288 1,167 - 16,732 - - - - 540 81,942,643 9,045,446 15,375,973 6,871,427 233,220,943 2,023,410 8,894,837 21 186,106,493 Institutions Under the Control of the Iowa Department of Human Services General Fund Expenditures by Institution (Unaudited) Year ended June 30, 2010 Me ntal He alth Me ntal He alth Me ntal He alth Me ntal He alth Pe rsonal se rvice s $ Woodward Institute - Institute - Institute - Institute - Re source Clarinda Mt. Ple asant Che roke e Inde pe nde nce Ce nte r 7,250,076 6,921,068 13,496,617 18,320,418 50,362,160 52,181 77,156 59,239 78,724 1,159,313 Supplie s and mate rials 652,037 490,945 1,075,399 777,745 4,726,391 Contractual se rvice s 594,108 914,448 1,202,746 2,122,178 7,172,716 42,725 183,274 121,510 86,222 1,742,716 Claims and misce llane ous 225 331 1,688 1,690 99,756 Lice nse s, pe rmits and re funds 466 - 895 2,565 528 - 1,183 - - - 8,591,818 8,588,405 15,958,094 21,389,542 65,263,580 Trave l Capital outlay Aid to individuals Total $ Re allocate d support se rvice s costs (se e page 6) (2,776,626) Total $ 13,181,468 22 Schedule 5 State State Civil Gle nwood Juve nile Training Commitme nt Re source Home - School - Unit for Se xual Ce nte r Tole do Eldora Offe nde rs Total 61,197,320 7,198,717 11,598,464 5,900,877 1,079,322 70,078 100,344 10,653 2,687,010 6,130,446 671,346 579,128 729,698 15,833,135 9,275,428 653,344 1,552,170 267,289 23,754,427 2,704,880 49,760 214,712 9,050 5,154,849 573,001 3,765 13,260 146 693,862 3,354 2,026 3,343 - 13,177 - - - - 1,183 80,963,751 8,649,036 14,061,421 6,917,713 230,383,360 2,776,626 9,694,339 23 182,245,717 Institutions Under the Control of the Iowa Department of Human Services General Fund Expenditures by Institution (Unaudited) Year ended June 30, 2011 Me ntal He alth Me ntal He alth Pe rsonal se rvice s $ Me ntal He alth Me ntal He alth Woodward Institute - Institute - Institute - Institute - Re source Clarinda Mount Ple asant Che roke e Inde pe nde nce Ce nte r 7,216,774 6,796,196 11,634,175 17,158,403 22,401 10,006 55,509 27,055 380,352 Supplie s and mate rials 523,233 461,404 905,510 799,733 4,479,918 Contractual se rvice s 498,036 1,025,590 1,399,542 2,091,352 4,809,727 34,698 159,299 144,081 318,639 804,932 54 58 1,165 945 108,933 425 - 780 2,077 985 - 2,293 - - - 8,295,621 8,454,846 14,140,762 20,398,204 60,672,788 Trave l Capital outlay Claims and misce llane ous Lice nse s, pe rmits and re funds Aid to individuals Total be fore re allocations $ Re allocate d support se rvice s costs (se e page 6) (2,757,545) Total $ 11,383,217 24 50,087,941 Schedule 6 State State Civil Gle nwood Juve nile Training Commitme nt Re source Home - School - Unit for Se xual Ce nte r Tole do Eldora Offe nde rs Total 61,427,351 7,022,669 11,085,766 6,124,755 692,274 11,896 37,574 63,732 1,300,799 6,712,830 678,049 624,520 799,415 15,984,612 8,264,636 682,848 1,333,028 180,936 20,285,695 1,453,278 77,944 167,607 47,202 3,207,680 506,136 1,980 12,745 825 632,841 4,584 595 3,958 - 13,404 - - - - 2,293 79,061,089 8,475,981 13,265,198 7,216,865 219,981,354 2,757,545 9,974,410 25 178,554,030 Institutions Under the Control of the Iowa Department of Human Services Resident/Patient Population Statistics (Unaudited) Year ended June 30, 2011 Population be ginning of year Me ntal Me ntal Me ntal He alth He alth He alth Me ntal He alth Woodward Institute - Institute - Institute - Institute - Re source Clarinda Mt. Ple asant Che roke e Inde pe nde nce Ce nte r 45 64 30 63 203 105 616 274 130 9 70 152 155 109 - Home visits - 1 - 205 - Limite d le ave s - - - 2 49 Te mporary me dical transfe rs - 6 - 16 - Unauthorize d de parture s - 2 - 1 - 175 777 429 463 58 184 760 429 239 15 4 Admissions: First admissions Re admissions Re turns: Total admissions Re le ase d: Discharges De aths - - - - Home visits - 1 - 205 - Limite d le ave s - - - 3 49 Te mporary me dical transfe rs - 8 3 16 - Unauthorize d de parture s - 11 - 2 - Othe r - - - - - 184 780 432 465 68 Population e nd of year 36 61 27 61 193 Ave rage numbe r of re side nts/patie nts 40 63 27 59 201 Total re le ase d 26 Schedule 7 State State Civil Gle nwood Juve nile Training Commitme nt Re source Home - School - Unit for Se xual Ce nte r Tole do Eldora Offe nde rs 289 76 129 80 4 67 250 4 4 - 8 - 409 - - - - - - - 165 - - - - - - - 582 67 258 4 14 91 108 1 6 - - - 409 - - - - - - - 165 - - - - - - - - - 149 - 594 91 257 1 277 52 130 83 286 60 143 81 27 Findings and Recommendations for Mental Health Institute - Clarinda June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Findings Reported in the State’s Report on Internal Control: No matters were noted. Other Findings Related to Internal Control: (1) Segregation of Duties – One important aspect of internal control is the segregation of duties among employees to prevent an individual employee from handling duties which are incompatible. When duties are properly segregated, the activities of one employee act as a check of those of another. Mail is not opened and distributed by someone other than accounting personnel. A list of receipts is not prepared by the mail opener. Responsibilities for collection and deposit preparation functions are not segregated from those for recording and accounting for cash receipts for the Sales and Collection, Contingent Fund, Patient and Entertainment Funds. Bank reconciliations are not reviewed by an independent person or there was no written evidence of who performed the independent review. Recommendation – We realize segregation of duties is difficult with a limited number of office employees. However, the Institution should review its control procedures to obtain the maximum internal control possible under the circumstances utilizing currently available personnel. Response – The Institution will continue to review its internal control policies, including utilization of staff outside the business office to assist in recording and accounting for cash receipts. Conclusion – Response accepted. (2) Bank Reconciliations – Monthly bank to book reconciliations were not performed timely and reconciliations are not reviewed by an independent person. Recommendation – Proper book to bank reconciliation procedures should be performed timely as a control over cash reporting. The reconciliations should be reviewed by an independent person and the reviews should be evidenced by the reviewer’s signature or initials and the date reviewed. Response – The Institution is in the process of reviewing our banking procedures and will include a review of the bank reconciliations in the changes we are making to the procedures. Conclusion – Response accepted. (3) Capital Assets – Chapter 7A.30 of the Code of Iowa requires each agency of the state to maintain a written, detailed and up-to-date inventory of property under its charge, control and management. The Institution is required to keep an up-to-date and accurate asset listing to track and maintain control over capital assets. This includes properly classifying additions and deletions for equipment and vehicles throughout the fiscal year, making additions and deletions to the capital asset listing and ensuring items are properly tagged. 28 Findings and Recommendations for Mental Health Institute - Clarinda June 30, 2011 The following items were noted: There is no written guideline for cost allocation of assets between Clarinda MHI and Clarinda Department of Corrections (DOC) identifying whether the asset belongs to the MHI or the DOC. One asset tested did not have a State tag ID affixed to the asset. Recommendation – The Institution should establish guidelines for cost allocation and identifying capital assets between Clarinda MHI and Clarinda DOC. The Institution should review policies and procedures to ensure all applicable capital assets purchased and maintained are properly tagged with the State tag ID number. Response – The Institution will review its policies for capital assets; including the cost allocation of capital assets. We will also review our policy on tagging assets; particularly those in areas not suited for paper tags. Conclusion – Response accepted. (4) Cancelling Supporting Documentation – Supporting documentation for 17 of 23 items was not cancelled to prevent reuse. Recommendation – The Institution should establish policies and procedures to require and ensure supporting documentation is properly cancelled to prevent reuse Response – The Institution will review its payment and revenue processes to include cancelling all supporting documentation. Conclusion – Response accepted. Findings Related to Statutory Requirements and Other Matters: No matters were noted. Staff: Questions or requests for further assistance should be directed to: Marlys K. Gaston, CPA, Manager Tracey L. Gerrish, Staff Auditor Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Ryan T. Jelsma, Staff Auditor Cory A. Lee, Assistant Auditor Jamie T. Reuter, Assistant Auditor 29 Findings and Recommendations for Mental Health Institute – Mount Pleasant June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Findings Reported in the State’s Report on Internal Control: No matters were noted. Other Findings Related to Internal Control: Capital Assets – Chapter 7A.30 of the Code of Iowa requires each agency of the state to maintain a written, detailed and up-to-date inventory of property under its charge, control and management. The Institution is required to keep an up-to-date and accurate capital asset listing to track and maintain control over capital assets. This includes properly classifying additions and deletions for equipment and vehicles throughout the fiscal year, making additions and deletions to the capital asset listing and ensuring items are properly tagged. Four assets did not have State tags affixed to them. Recommendation – The Institution should review policies and procedures to ensure all applicable capital assets purchased and maintained are properly tagged with the State ID number. Response – The Institution will ensure all applicable capital assets purchased and maintained by the Institution are properly tagged with a State ID number. Conclusion – Response accepted. Findings Related to Statutory Requirements and Other Matters: No matters were noted. Staff: Questions or requests for further assistance should be directed to: Brian R. Brustkern, CPA, Manager Scott P. Boisen, Senior Auditor II Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Tyler L. Carter, Staff Auditor James H. Pitcher, Staff Auditor Russell G. Jordan, CPA, Assistant Auditor Eric L. Rath, Assistant Auditor W. Brad Corley, Assistant Auditor 30 Findings and Recommendations for Mental Health Institute - Cherokee June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Findings Reported in the State’s Report on Internal Control: No matters were noted. Other Findings Related to Internal Control: No matters were noted. Findings Related to Statutory Requirements and Other Matters: No matters were noted. Staff: Questions or requests for further assistance should be directed to: Deborah J. Moser, CPA, Manager Kelly L. Hilton, Staff Auditor Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Brett A. Hoffman, Staff Auditor Hannah K. Haas, Assistant Auditor Marijke J. Hodgson, Assistant Auditor Andi J. Kaufman, CPA, Assistant Auditor Jamie T. Reuter, Assistant Auditor 31 Findings and Recommendations for Mental Health Institute - Independence June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Findings Reported in the State’s Report on Internal Control: No matters were noted. Other Findings Related to Internal Control: Eligibility – Title XIX – The Institution is required to maintain patient files, including documentation of patient eligibility for Title XIX funding which can be in a paper or electronic format. Patient files did not contain evidence of proper determination of eligibility, including reviews for continued eligibility during the fiscal year ended June 30, 2011. Documentation for patient eligibility was subsequently obtained in order to bill for services. Recommendation - The Institution should maintain patient files, including documentation of patient eligibility for Title XIX funding, on a current basis. Response - The Institution will comply with the recommendation. During the fiscal year ended June 30, 2010, the Institution’s only Income Maintenance Worker separated employment under the State Employee Retirement Incentive Program (SERIP). This position was not immediately replaced. An Income Maintenance Worker was added to the Institution staff during the fiscal year ended June 30, 2011 and has been maintaining required documentation since then. This employee was also able to retrospectively establish eligibility for Title XIX and update the patient files accordingly. Conclusion – Response accepted. Findings Related to Statutory Requirements and Other Matters: No matters were noted. Staff: Questions or requests for further assistance should be directed to: Suzanne R. Dahlstrom, CPA, Manager Darryl J. Brumm, CPA, Senior Auditor II Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Kelly L. Hilton, Staff Auditor Brett A. Hoffman, Staff Auditor Ryan T. Jelsma, Staff Auditor James H. Pitcher, Staff Auditor Emily K. Creighton, Assistant Auditor Karie A. Meisgeier, CPA, Assistant Auditor Andi J. Kaufman, CPA, Assistant Auditor 32 Findings and Recommendations for Woodward Resource Center June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Finding Reported in the State’s Report on Internal Control: No matters were noted. Other Findings Related to Internal Control: (1) Capital Assets – Chapter 7A.30 of the Code of Iowa requires each agency to maintain a written, detailed and up-to-date inventory of property under its charge and control. One asset selected from the capital asset listing could not be located because the asset was disposed of during the year, causing assets and accumulated depreciation to be overstated by $17,100. Recommendation – The Center should implement procedures to ensure the capital asset listing is current and accurate. Response – Woodward Resource Center acknowledges one item tested did not exist and was on the capital asset listing, but has now been deleted. Conclusion – Response accepted. (2) Reconciliation of Medicare D Billings – A reconciliation of Medicare D billings to payments received is not performed. Recommendation – A reconciliation of Medicare D billings to payments received should be performed monthly to detect and correct billing errors. Response – Woodward Resource Center will move forward with having the Pharmacy provide the Business Office with a report to use for reconciling the billings and payments. Conclusion – Response accepted. Findings Related to Statutory Requirements and Other Matters: Employee Evaluations – Annual employee performance evaluations should be performed. Three of ten employees tested did not have a current performance evaluation in his or her personnel file. Recommendation – The Center should implement procedures to ensure employee performance evaluations are performed annually. Response – This has been corrected and reviewed with all supervisors at Woodward Resource Center. Conclusion – Response accepted. 33 Findings and Recommendations for Woodward Resource Center June 30, 2011 Staff: Questions or requests for further assistance should be directed to: Michelle B. Meyer, CPA, Manager Casey L. Johnson, Staff Auditor Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Janet K. Mortvedt, CPA, Senior Auditor Leanna J. Showman, Staff Auditor Nancy J. Umsted, Assistant Auditor Jamie T. Reuter, Assistant Auditor Victor L. Kennedy, Assistant Auditor 34 Findings and Recommendations for Glenwood Resource Center June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Findings Reported in the State’s Report on Internal Control: No matters were noted. Other Findings Related to Internal Control: No matters were noted. Findings Related to Statutory Requirements and Other Matters: No matters were noted. Staff: Questions or requests for further assistance should be directed to: Deborah J. Moser, CPA, Manager Marta M. Sobieszkoda, Staff Auditor Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Gabriel M. Stafford, CPA, Staff Auditor Robert W. Endriss, Assistant Auditor Adam B. Bartz, Assistant Auditor Victor L. Kennedy, Assistant Auditor Jason Ropte, Auditor Intern 35 Findings and Recommendations for State Juvenile Home - Toledo June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Findings Reported in the State’s Report on Internal Control: No matters were noted. Other Findings Related to Internal Control: No matters were noted. Findings Related to Statutory Requirements and Other Matters: No matters were noted. Staff: Questions or requests for further assistance should be directed to: Brian R. Brustkern, CPA, Manager Jenny R. Lawrence, Staff Auditor Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Leanna J. Showman, Staff Auditor Ryan T. Jelsma, Staff Auditor Marijke Hodgson, Assistant Auditor Andi J. Kaufman, CPA, Assistant Auditor Stephen J. Hoffman, Auditor Intern 36 Findings and Recommendations for State Training School - Eldora June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Findings Reported in the States Report on Internal Control: No matters were noted. Other Finding Related to Internal Control: Capital Assets - The State Training School sold four vehicles during fiscal year 2011. However, the gain on sale was incorrectly calculated and was overstated by $4,822.14 on the GAAP package. Also, the current year depreciation was overstated by $139,198.08. In addition, a prior year correction of $7,510.09 for accumulated depreciation was not included in the current year, resulting in a total accumulated depreciation overstatement of $146,708.17 on the GAAP package. Recommendation – Chapter 7A.30 of the Code of Iowa requires each agency of the state to maintain a written, detailed and up-to-date inventory of property under its charge and control. Accumulated depreciation and any gains on sale of equipment should be properly computed and reported on the GAAP package. Capital asset records should be updated to adjust for these corrections. Response – The business office staff shall make the recommended corrections to the capital asset records in the GAAP package. Even though the GAAP package was meticulously reviewed by the available staff, this review process missed the overstatement of depreciation and the error in accumulated depreciation. The State Training School shall incorporate additional reviews which will help ensure GAAP package reporting is as error free as possible. Conclusion – Response accepted. Finding Related to Statutory Requirements and Other Matters: No matters were noted. Staff: Questions or requests for further assistance should be directed to: Brian R. Brustkern, CPA, Manager Brett A. Hoffman, Staff Auditor Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Justin M. Scherrman Staff Auditor Kelly L. Hilton, Staff Auditor Adam B. Bartz, Assistant Auditor Laura E. Grinnell, Assistant Auditor Cory A. Lee, Assistant Auditor 37 Findings and Recommendations for Civil Commitment Unit for Sexual Offenders - Cherokee June 30, 2011 Findings Reported in the State’s Single Audit Report: No matters were noted. Findings Reported in the State’s Report on Internal Control: No matters were noted. Other Findings Related to Internal Control: No matters were noted. Findings Related to Statutory Requirements and Other Matters: No matters were noted. Staff: Questions or requests for further assistance should be directed to: Deborah J. Moser, CPA, Manager Kelly L. Hilton, Staff Auditor Andrew E. Nielsen, CPA, Deputy Auditor of State Other individuals who participated in the audits include: Brett A. Hoffman, Staff Auditor Andi J. Kaufman, CPA, Assistant Auditor 38