Taser Intl Responds to New York Post, Taser Intl, 2002

Download original document:

Document text

Document text

This text is machine-read, and may contain errors. Check the original document to verify accuracy.

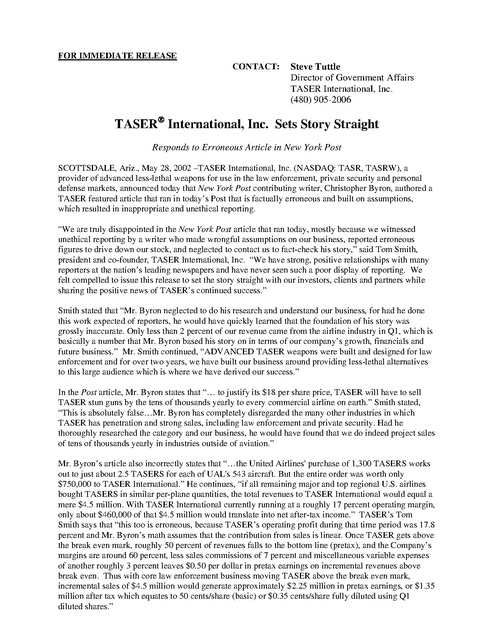

FOR IMMEDIATE RELEASE CONTACT: Steve Tuttle Director of Government Affairs TASER International, Inc. (480) 905-2006 TASER® International, Inc. Sets Story Straight Responds to Erroneous Article in New York Post SCOTTSDALE, Ariz., May 28, 2002 –TASER International, Inc. (NASDAQ: TASR, TASRW), a provider of advanced less-lethal weapons for use in the law enforcement, private security and personal defense markets, announced today that New York Post contributing writer, Christopher Byron, authored a TASER featured article that ran in today’s Post that is factually erroneous and built on assumptions, which resulted in inappropriate and unethical reporting. “We are truly disappointed in the New York Post article that ran today, mostly because we witnessed unethical reporting by a writer who made wrongful assumptions on our business, reported erroneous figures to drive down our stock, and neglected to contact us to fact-check his story,” said Tom Smith, president and co-founder, TASER International, Inc. “We have strong, positive relationships with many reporters at the nation’s leading newspapers and have never seen such a poor display of reporting. We felt compelled to issue this release to set the story straight with our investors, clients and partners while sharing the positive news of TASER’s continued success.” Smith stated that “Mr. Byron neglected to do his research and understand our business, for had he done this work expected of reporters, he would have quickly learned that the foundation of his story was grossly inaccurate. Only less than 2 percent of our revenue came from the airline industry in Q1, which is basically a number that Mr. Byron based his story on in terms of our company’s growth, financials and future business.” Mr. Smith continued, “ADVANCED TASER weapons were built and designed for law enforcement and for over two years, we have built our business around providing less-lethal alternatives to this large audience which is where we have derived our success.” In the Post article, Mr. Byron states that “… to justify its $18 per share price, TASER will have to sell TASER stun guns by the tens of thousands yearly to every commercial airline on earth.” Smith stated, “This is absolutely false…Mr. Byron has completely disregarded the many other industries in which TASER has penetration and strong sales, including law enforcement and private security. Had he thoroughly researched the category and our business, he would have found that we do indeed project sales of tens of thousands yearly in industries outside of aviation.” Mr. Byron’s article also incorrectly states that “…the United Airlines' purchase of 1,300 TASERS works out to just about 2.5 TASERS for each of UAL's 543 aircraft. But the entire order was worth only $750,000 to TASER International.” He continues, “if all remaining major and top regional U.S. airlines bought TASERS in similar per-plane quantities, the total revenues to TASER International would equal a mere $4.5 million. With TASER International currently running at a roughly 17 percent operating margin, only about $460,000 of that $4.5 million would translate into net after-tax income.” TASER’s Tom Smith says that “this too is erroneous, because TASER’s operating profit during that time period was 17.8 percent and Mr. Byron’s math assumes that the contribution from sales is linear. Once TASER gets above the break even mark, roughly 50 percent of revenues falls to the bottom line (pretax), and the Company’s margins are around 60 percent, less sales commissions of 7 percent and miscellaneous variable expenses of another roughly 3 percent leaves $0.50 per dollar in pretax earnings on incremental revenues above break even. Thus with core law enforcement business moving TASER above the break even mark, incremental sales of $4.5 million would generate approximately $2.25 million in pretax earnings, or $1.35 million after tax which equates to 50 cents/share (basic) or $0.35 cents/share fully diluted using Q1 diluted shares.” Mr. Byron continues with more erroneous assumptions in his article where he states that “With 3.8 million shares currently outstanding, this bottom line income would translate into net earnings of roughly 12 cents per share, meaning that at the stock's current price of $18, the shares are trading at 150 times earnings from a one-time set of contract sales that may actually never take place at all.” Again, as Smith details, “This is incorrect because it ignores our core business. In the first quarter of this year, the airlines accounted for less than 2 percent of sales - $45,000 out of $2.3 million were airlines - and the remainder or 98 percent came from our core law enforcement and other security markets.” Smith continues, “We attribute this success to the efficacy of and demand for our product.” Other errors in Mr. Byron’s article include these excerpts: “In other words, with each $575 TASER generating a tiny fraction of a cent per share of earnings, TASER International will have to sell roughly 44,000 TASERS yearly - which means three TASERS for every commercial aircraft in the skies, worldwide - simply to be valued at the 37.5 times current earning multiple at which it traded last summer before the 9/11 panic distorted everything.” “Unfortunately, Mr. Byron’s math is again wrong as exampled by this statement,” stated Smith. “If we assume 44,000 TASERS sold at $575 equals $25.3 million and using our pre-tax income of $8.65 million, then the outcome would actually generate earnings of $5.2 million. In reality, there are only 2.8 million (basic) shares outstanding and 3.8 million fully diluted shares so this would equate to earnings of $1.85 per share (basic) and $1.37 per share fully diluted, or a price earnings ratio of only 9.7 (basic) and 13.1 fully diluted (assuming $18 per share market price), not 37.5. Again, this is another bogus calculation.” Regarding Mr. Byron’s statement, “the 37.5 multiple is itself obviously too high. With the 30 stocks of the Dow industrials now selling for 20 times year-ahead earnings, a good argument can be made that TASER International will have to sell more than 100,000 stun guns yearly to justify its current price” is also off base according to Smith. Smith states that “Dow industrials sell at 20 times earnings because they are mature industries, and none of these companies are experiencing year over year 100 percent growth. To compare our P/E to the Dow is fundamentally ridiculous, because we are projecting earnings of $0.50 this year based on our guidance which would lead to a P/E ratio of 36 at $18 per share. A 36 P/E is not unreasonable for a company with 100 percent annual growth top and bottom line…especially since earnings should grow faster than revenues for growth companies because of the extra investments in early years required to build markets.” Mr. Byron also concedes in brief that “bulls on the stock are now talking up the earth-bound market for the guns …but all of that is just hopeful thinking to justify the price run-up that is simply not supported by the market potential that caused the surge in the first place.” However Smith states, “In actuality, the opposite is true. TASER management has consistently focused on its core markets, especially law enforcement. The improvement in our stock price has been due to the overall success of our business, not publicity relating to airline security. There are approximately 10-12 million police officers worldwide and 30-35 million private security guards worldwide, and being very conservative with the number of over 50 million consumers worldwide supporting a tremendous opportunity for TASER International. Mr. Byron's assumptions also completely disregard the recurring annual revenue that will be generated from the weapon’s Air Cartridge sales. Annual training for law enforcement officers and private security guards will only continue to increase the demand on the disposable Air Cartridge as more and more of the ADVANCED TASERs are sold in this marketplace.” For additional facts and perspective from TASER International, Mr. Smith will be available for interviews to continue to clarify and correct the erroneous article written by Christopher Byron. About TASER International, Inc. TASER International, Inc. provides advanced less-lethal weapons for use in the law enforcement, private security, and personal defense markets. Its flagship ADVANCED TASER® product uses proprietary technology to incapacitate dangerous, combative, or high-risk subjects that may be impervious to other less-lethal means. This technology reduces injury rates to suspects and officers, thereby lowering liability risk and improving officer safety. The ADVANCED TASER is currently in testing or deployment at over 1400 law enforcement and correctional agencies in the U.S. and Canada. Certain statements contained in this document may be deemed to be forward-looking statements as defined by the Private Securities Litigation Reform Act of 1995, and TASER International intends that such forward-looking statements be subject to the safe-harbor created thereby. Such forward-looking statements relate to: 1) expected revenue and earnings growth; 2) the Company’s estimates regarding the size of its target markets; 3) the ability of TASER to successfully penetrate the law enforcement market; 4) the growth expectations for existing accounts; 5) the ability of TASER to expand its product sales to the private security, military and consumer self-defense markets; and 6) the Company’s target business model. TASER cautions that these statements are qualified by important factors that could cause actual results to differ materially from those reflected by the forward-looking statements herein. Such factors include, but are not limited to: 1) market acceptance of the Company’s products; 2) TASER’s ability to establish and expands its direct and indirect distribution channels; 3) TASER’s ability to attract and retain the endorsement of key opinion-leaders in the law enforcement community; 4) the level of product technology and price competition for the Company’s Advanced TASER product; 5) the degree and rate of growth of the markets in which TASER competes and the accompanying demand for its products; and 6) other factors detailed in the Company’s filings with the Securities and Exchange Commission. ###