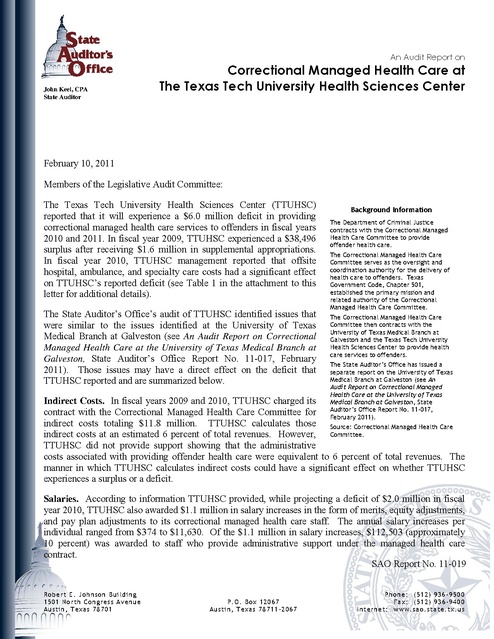

Texas Audit Tdcj Medical Care 2011

Download original document:

Document text

Document text

This text is machine-read, and may contain errors. Check the original document to verify accuracy.

An Audit Report on

John Keel, CPA

State Auditor

Correctional Managed Health Care at

The Texas Tech University Health Sciences Center

February 10, 2011

Members of the Legislative Audit Committee:

The Texas Tech University Health Sciences Center (TTUHSC)

reported that it will experience a $6.0 million deficit in providing

correctional managed health care services to offenders in fiscal years

2010 and 2011. In fiscal year 2009, TTUHSC experienced a $38,496

surplus after receiving $1.6 million in supplemental appropriations.

In fiscal year 2010, TTUHSC management reported that offsite

hospital, ambulance, and specialty care costs had a significant effect

on TTUHSC’s reported deficit (see Table 1 in the attachment to this

letter for additional details).

The State Auditor’s Office’s audit of TTUHSC identified issues that

were similar to the issues identified at the University of Texas

Medical Branch at Galveston (see An Audit Report on Correctional

Managed Health Care at the University of Texas Medical Branch at

Galveston, State Auditor’s Office Report No. 11-017, February

2011). Those issues may have a direct effect on the deficit that

TTUHSC reported and are summarized below.

Background Information

The Department of Criminal Justice

contracts with the Correctional Managed

Health Care Committee to provide

offender health care.

The Correctional Managed Health Care

Committee serves as the oversight and

coordination authority for the delivery of

health care to offenders. Texas

Government Code, Chapter 501,

established the primary mission and

related authority of the Correctional

Managed Health Care Committee.

The Correctional Managed Health Care

Committee then contracts with the

University of Texas Medical Branch at

Galveston and the Texas Tech University

Health Sciences Center to provide health

care services to offenders.

The State Auditor’s Office has issued a

separate report on the University of Texas

Medical Branch at Galveston (see An

Audit Report on Correctional Managed

Health Care at the University of Texas

Medical Branch at Galveston, State

Auditor’s Office Report No. 11-017,

February 2011).

Indirect Costs. In fiscal years 2009 and 2010, TTUHSC charged its

contract with the Correctional Managed Health Care Committee for

indirect costs totaling $11.8 million. TTUHSC calculates those Source: Correctional Managed Health Care

indirect costs at an estimated 6 percent of total revenues. However, Committee.

TTUHSC did not provide support showing that the administrative

costs associated with providing offender health care were equivalent to 6 percent of total revenues. The

manner in which TTUHSC calculates indirect costs could have a significant effect on whether TTUHSC

experiences a surplus or a deficit.

Salaries. According to information TTUHSC provided, while projecting a deficit of $2.0 million in fiscal

year 2010, TTUHSC also awarded $1.1 million in salary increases in the form of merits, equity adjustments,

and pay plan adjustments to its correctional managed health care staff. The annual salary increases per

individual ranged from $374 to $11,630. Of the $1.1 million in salary increases, $112,503 (approximately

10 percent) was awarded to staff who provide administrative support under the managed health care

contract.

SAO Report No. 11-019

~

r

Robert E. Johnson Building

1501 North Congress Avenue

Austin, Texas 78701

r

P.O. Box 12067

Austin, Texas 78711 -20 67

Phone: (512) 936 -950 0

Fax: (512) 93 6-9400

Internet: www.sao.state.tx.u s

Members of the Legislative Audit Committee

February 10, 2011

Page 2

Allowable Costs. TTUHSC had support for almost all expenditures auditors tested related to the reported

deficits. However, in fiscal year 2010, TTUHSC’s correctional managed health care unit (TTUHSC-CMC

Division) spent at least $52,465 for employee benefits not authorized by the contract. (See Section 4 of the

attachment to this letter for auditors’ methodology for auditing employee benefits.) Due to a lack of clear

guidance in the contract between TTUHSC and the Correctional Managed Health Care Committee, auditors

were unable to determine whether $159,082 in fiscal year 2010 expenditures were reasonable and necessary

to providing offender health care.

Reimbursement Amounts. The majority of TTUHSC’s expenditures related to offender health care are

associated with TTUHSC’s contracts with medical facilities or medical professionals. The contracts specify

agreed-upon reimbursement amounts for providing services. For example:

TTUHSC has 213 offsite professional services contracts through which providers offer offender health

care. TTUHSC reimburses approximately 67 percent of those 213 providers based on the Medicare fee

schedule.

TTUHSC reimburses most offsite hospitals or facilities with which it contracts to provide offender

health care at rates based on the Medicare fee schedule.

TTUHSC reimburses nine local community hospitals with which it contracts to provide onsite health

care to offenders at capitated rates that range from $1.86 to $3.57 per patient per day.

Organizational Structure. TTUHSC has established TTUHSC-CMC Division as a department within

TTUHSC. That department operates under the direction of an executive director of administration and an

executive medical director. The Correctional Managed Health Care Committee does not participate in the

day-to-day operations of providing offender health care at TTUHSC. (See Section 2 of the attachment to

this letter for an organizational chart.)

In a 2007 report1, the State Auditor’s Office recommended that TTUHSC continue its efforts to replace its

existing financial management system with a new system. TTUHSC implemented a new financial

accounting system in September 2008.

The information systems TTUHSC uses to report information and generate financial reports on correctional

managed health care are generally secure and provide complete and accurate information. However,

TTUHSC does not maintain documentation to support the test results for the procedures it performed on

certain information systems prior to implementation and upgrade.

1

See An Audit Report on Correctional Managed Health Care Funding Requirements, State Auditor’s Office Report No. 07-017, March 2007.

Members of the Legislative Audit Committee

February 10, 2011

Page 3

Recommendations

TTUHSC should:

Maintain documentation to support indirect costs for offender health care and ensure that it charges only

reasonable and authorized direct and indirect expenditures to its contract with the Correctional Managed

Health Care Committee.

Obtain approval from the Legislative Budget Board before charging any indirect costs to TTUHSCCMC Division and using funds appropriated for the purpose of providing offender health care to cover

those costs.

Seek prior approval from the Correctional Managed Health Care Committee and/or the Legislative

Budget Board before TTUHSC-CMC Division awards salary increases to its employees using funds

appropriated for offender health care.

Ensure transparency in its process for determining reimbursement amounts for professional services,

local community hospitals, and other contracted hospital services by annually providing proposed

reimbursement amounts, the methodology applied, and related supporting documentation to:

The executive director of the Correctional Managed Health Care Committee for review and written

approval.

The Health and Human Services Commission’s rate-setting division for its review and comment.

The Legislative Budget Board for its review and written approval prior to expending any

appropriated funds for the purpose of providing offender health care.

Maintain documentation for the test results of procedures performed for certain information systems

prior to implementation and upgrade.

The Legislature may consider requiring TTUHSC to:

Annually obtain a review of reimbursement amounts from the Health and Human Services

Commission’s rate-setting division and from the Legislative Budget Board.

Annually obtain written approval from the Legislative Budget Board before implementing TTUHSCCMC Division reimbursement amounts.

Publish proposed TTUHSC-CMC Division reimbursement amounts, rates, and the associated

methodology in the Texas Register.

The Legislature also may wish to consider determining the extent to which or whether TTUHSC-CMC

Division’s funds appropriated for offender health care should be used to pay indirect costs.

Members of the Legislative Audit Committee

February 10, 2011

Page 4

TTUHSC management did not agree with the recommendations in this report, and its detailed response is

presented in Section 3 of the attachment to this letter. The information in TTUHSC’s management’s

response did not cause the State Auditor’s Office to modify the issues or recommendations in this report. If

you have any questions, please contact Nicole Guerrero, Audit Manager, or me at (512) 936-9500.

Sincerely,

John Keel, CPA

State Auditor

Attachment

cc:

Members of the Texas Tech University System Board of Regents

Mr. Larry K. Anders, Chair

Mr. Jerry E. Turner, Vice Chair

Mr. L. Frederick Francis

Mr. Jeff Harris

Mr. John Huffaker

Mr. Mickey L. Long

Ms. Debbie Montford

Ms. Nancy Neal

Mr. John F. Scovell

Mr. Daniel T. Serna

Mr. Kent Hance, Chancellor, Texas Tech University System

Dr. Tedd Mitchell, President, Texas Tech University Health Sciences Center

Members of the Correctional Managed Health Care Committee

Dr. James D. Griffin, Chair

Mr. Elmo Cavin

Mr. Bryan Collier

Mr. William Elger

Mr. Gerald Evenwel, Jr.

Dr. Cynthia Jumper

Dr. Lannette Linthicum

Dr. Ben G. Raimer

Dr. Desmar Walkes

Mr. Allen Hightower, Executive Director, Correctional Managed Health Care Committee

This document is not copyrighted. Readers may make additional copies of this report as needed. In

addition, most State Auditor’s Office reports may be downloaded from our Web site:

www.sao.state.tx.us.

In compliance with the Americans with Disabilities Act, this document may also be requested in

alternative formats. To do so, contact our report request line at (512) 936-9500 (Voice), (512) 936-9400

(FAX), 1-800-RELAY-TX (TDD), or visit the Robert E. Johnson Building, 1501 North Congress Avenue, Suite

4.224, Austin, Texas 78701.

The State Auditor’s Office is an equal opportunity employer and does not discriminate on the basis of

race, color, religion, sex, national origin, age, or disability in employment or in the provision of services,

programs, or activities.

To report waste, fraud, or abuse in state government call the SAO Hotline: 1-800-TX-AUDIT.

Attachment

Section 1

TTUHSC Correctional Managed Health Care Expenditures for Fiscal

Years 2009 and 2010

Table 1 shows Texas Tech University Health Sciences Center’s (TTUHSC)

correctional managed health care expenditures for fiscal years 2009 and 2010.

Table 1

TTUHSC Correctional Managed Health Care Expenditures

Fiscal Years 2009 and 2010

Fiscal Year 2009

Expenditure Category

Expenditures

Fiscal Year 2010

Percent of

Total

Expenditures

Expenditures

Percent of

Total

Expenditures

Totals for

Fiscal Years

2009 and

2010

Salaries

$ 29,862,758

29.57%

$ 32,662,091

29.76%

$ 62,524,849

Benefits

7,210,003

7.14%

7,708,921

7.02%

14,918,924

Operating Expenditures

(Maintenance and

Operations)

3,438,278

3.40%

2,766,681

2.52%

6,204,959

Professional Services

6,707,716

6.64%

7,058,522

6.43%

13,766,238

23,660,936

23.43%

24,551,003

22.37%

48,211,939

Travel

179,349

0.18%

188,504

0.17%

367,853

Electronic Medicine

(Telemedicine/EMR)

315,274

0.31%

371,697

0.34%

686,971

Capital Equipment

Exceeding $5,000

411,675

0.41%

370,010

0.34%

781,685

0

0.00%

0

0.00%

$0

Indirect Expenses

5,701,280

5.65%

6,133,412

5.59%

11,834,692

Pharmaceutical Purchases

(Drug Costs)

6,859,760

6.79%

7,605,150

6.93%

14,464,910

962,023

0.95%

1,122,476

1.02%

2,084,499

15,421,674

15.27%

18,904,415

17.22%

34,326,089

250,000

0.25%

325,000

0.30%

575,000

$109,767,882

100.00%

$210,748,608

Contracted Units/Services

Depreciation

University Professional

Services

Freeworld Provider

Services

Estimated Incurred But

Not Reported (IBNR)

Expenditures

Totals

$100,980,726

100.00%

a

Source: Information provided by TTUHSC.

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 1

Section 2

Organizational Chart for TTUHSC Correctional Managed Health Care

Figure 1 shows the flow of funds from the Department of Criminal Justice to the Texas Tech

University Health Sciences Center (TTUHSC) and identifies the TTUHSC departments that

are involved in providing offender health care services. As of August 2010, the correctional

managed health care program at TTUHSC had approximately 685 filled, full-time positions.

Figure 1

Organizational Chart for TTUHSC Correctional Managed Health Care

Fiscal Year 2010

Department of Criminal

Justice

$466.4 million

Correctional Managed Health

Care Committee

Retains $0.7 million

(See Note 1)

Texas Tech University Health

Sciences Center

$99.6 million

Texas Tech University Health

Sciences Center

Dean of the School of

Medicine

Texas Tech University Health

Sciences Center

Associate Dean

Health Services Management

CMHC Executive Medical

Director

CMHC Executive Director

CMHC Medical

(includes Dental, Regional

Medical Directors and staff,

Nursing Services, Utilization

Management, and

Credentials Coordinator)

CMHC Administration

(Includes Field Operations,

CMHC Recruitment, CMHC

Mental Health System,

Regional Medical Facility,

Information Systems,

Finance and Administration,

and Human Resources)

(See Note 2)

(See Note 2)

Note 1: Of the $466.4 million it receives from the Department of Criminal Justice, the Correctional Managed Health Care Committee

retains $0.7 million for its operations, passes $99.6 million through to TTUHSC, and passes $366.1 million to the University of Texas

Medical Branch at Galveston.

Note 2: TTUHSC estimated its fiscal year 2010 salary costs would be approximately $23 million for CMHC Medical and approximately $8

million for CMHC Administration.

Source: Developed by auditors based on information provided by TTUHSC.

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 2

Section 3

Management’s Responses

1 XA

fECIi

NtVFRSITV

HEALTH SCIENCES CENTER

Office of the Pre..denr

.

Fehruary 7. 201 I

: tall' uduor"s Officc

I I 'Courtney \mhres- \Vade

P,O. B l, Ul67

uSlin. 1 78711-2067

Dear Ms,

mbres- Wade:

rhank you for the opportunily 10 re\ic\\ and re p nd 10 the draft repor! for the 'laIC uditor's

Omce (: 0) audit of orreclillnal Managed Ilealth arc til Ie, a. Iech LInivcrsil) 1Ic,Ilth

,dences enter (TIUII l, The respon es of our leadership ll:am arc II1cluded hclo\1

IndirecI ('osUi

In the ) loher 200(} audit related I

rrc lional managed health care, the. laIC udilor', fliel'

Issued thIS stah:ment encompas ing Tr II '. mcth dol g' for charging indlrecI ellst,. "The

inslillllioos' methodologies for calculating the indirect co 'IS aSSOCiated \1 uh prm idll1g health

care to tate pri on inmate' arc reaonahle .. We bdic\ e thUI the 6°" indirect Cl :1 rale i. fair and

reasonable. (The lillli (' federal government indirect cosl rate I. 41l.S" ) Included 111 the 6° 0

rate arc all the direci adminl.lrative ost of this contract. Hfecti\e wilh Ihe renewal oflhis

conlraCI on • eplember 1. _0 II, IT II 'V\ ill charge Ihesl: dIrect udmilllslrati\ e CIlSt. to the

contract. thereb) I wering the IIlt!lrecl COSI ratl: to t5° o. n llll: i 'urr>ntl) preparing Ih'

IIldlrect co't 'Iud)' Ii r lis al year _010 in nrder 10 supporl our rail' n.:newal wilh the federal

government. The results oflhis . Iud) will he :.l\ailahk tn documenllhe fact that an mdin,:cI CUI

rale ofl.S% for this contra 't i \\cll-juslllied.

\:'e reo re Ifully di agree with th' 'late uditor's recommendation lhat rr H.T gain appro\'al

from the Legi IUli\c Budgct Board (T RRl tor the indin: t co I ralc. a no su h requirement

currently cxi IS.

Salancs

Wc respcctfully disagrce \\ith the ,'lalC udilOr's ree 11lll1lCndattnn 10 :cd. pnur appro\,,1 from

the Correcli nol onoged Ilcalth arc ommillee ( tv 11 I C) and or Ihe I.HB bdim.: u\\arding

salar) incrca'e 10 our empll )ecs. (\ rre lional I\dUlgcd lIealth 'arc (C \111 ') al I Il II. C is a

di\'ision of the hool of tvlcdicine. and all it employec' arc cmplo)cc )1' I I LJII' . rhe

, hool of Medicine and 'Mlle arc go\'erned by all instilulil nal policie and guidelines of

n Llil. ',and \\C 10110\\ Instillltion:ll policic for salar) increa'e' I'llI' lIJ' • 111 'empltlyees

36014th treel STOP 6258

I Lubbock. Texa.

79430·6258

I T 806.7432900 II' 806.743.2910

An I::.EO, Altlnn.IU\lt.· Acuon Immullon

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 3

Page Iwo

lIowuble osts

e r pe tfull) di agree \\ iUl the tate uditor' s implications that 159,082 in Iiscal ) car 20 I0

e penditures ma) ha e been unreasonable or unnece 'ar) We believe all fthe expen e are

appropriate. allowable. and nece ar) 10 conduct day -to-day bU'ine 'rclated to pri 'on health

can: operations. Th' questioned expenditure include 0 t of recruitll1g h alth care candidate

and 0 t 0 cellular phone u ed dail. by ur empl yee in fulfilling the agreement vvith the

H '. The'e co 't. art: rt:3' nabk and required to conduct busincs and compete in the

recruitment of health care pr)\ idcrs out ide the correctional. y.-tern. dditionall). contract

langua 'e in rticle III 'cction L pro ides guidelin" on "Restri 'tions f r:xpenditures" for ur

correctional agrccment, and expenditures arc audited monthl b the 111

10 ensure

compliance \\ith the e requirement, \. uch. we di agr.:e that con ract c1anlic!lti n I: needed

TIle 52.46 in 'mplo ee b 'nelit the. tate \uditor a crt' arc n I auth riLed by the e I1traet

repre 'CIllS rctirernelll fringe benefit expen'e ' that arc not omplctcl relmbur. ed b fringe

rev nue credits, therefor re, ulting in a net expl:n, e un ler thl greem nl. I It .en r. I

ppr priation

t tate' that no IT II" higher cdueati n fund' 'hall be 'pent on the

correcti nal agreement. as rclcreneed in enate Bill I, 1'1 Legi lature. Jeneral ppropriation

ct. rticle III, page 192 #4 ppropriation of o. t for Ilealth ar' to Inmate', which ·tate '. "It

i the intent of the Legislature that all st f r providing health care to inmate of the TD J

in luding co t of operating

J h pital fa ilitie in ah eton • unt) and Lubbol:k 'ount

shalt be paid from appropriations made to the TD 'J," Durin I contract neg llati n. r the ne

bienniwlL rUll"

ill seek I, rifi ati n in ule 'Mlle' I II JJ J' agreement and

recommend appropriate changes to the section addres 'ing fringes to clarify this i sue and to be

con i tent with legislative intenl.

Reimbur. ement mounts

We re pectfult) disagree with the tate uditor' re ommendations lor TTUH

toeek

appro al from lIealth and lIuman 'r ice ommi ion and the Of) of th rates w' pay to 'ubsu h requirement urrentl e ists and implementing thi

ntra t health car providers.

re ommendati n w uld add to the admini 'trative co t thi' ntra I. I he

J I' appro\e

the e costs when the appro e lhe bienmal contract with I lUll: 'to deliver health care t the

II1mat p pulati n.

fhe current rate structure for offsite care (onsite 'pecialty ph) 'i ·ian. hospitali/tllion. and

ambulan e rvi c ) ha. igniti, ntly dis oUllled ntra t nd payment mechanism in pia e.

The 'Mil

urrcntl} m nit r' thee type' or e penditurc m nthl}. dditi n It)', the ,., c. I

hospital nsite contracts" refer to our contracts with local communit ho. pital' t operate 'ome

of our onsile pri on medical clinic. TIle e co t con i t mainly of alar)' and fringe. and

increase are gi en under the ame ir umstan e a raLe. for Trlll!.T cmplo ee..

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 4

Pa 'c rhrcc

Organwllion I tru tun:

We re 'pectfull) di agree \\ ilh!he tate udllor' . recommendation to ma1l1La1l1 d cumentatlon f

the test reult f pr cedure· perf, rmed pri r ( implementation and upgrade of information

stems. , preadshcets that wcre u ·cd during the "mo 1,." c. erci 'C 'pri r t implemcntati n and

prior t th upgrad were pr( \ Ided to the

(during the audit. Thc . pread heet utlined the

t . t pro cdurc. thaI were perf, mled pri r t implementati nand pn r to the upgrade.• u ceo .Iul

complcti n fall cnarios \~a<; enfied bcfore impl'menlati)l1, In our pll1l n. r~tall1lng le·t

r ult aft r implcm ntallon i unn 'ccssar)

If ou havc questi )I1S about our resp n c , plea.. ' fi 'I In: 'to '(Intact Ir. I Iml

\111. 1

·xecutivc Ice I rc Ident for I'manec and dmml. tratl n, r Ir. larr) U1,.1I1., I Il H,'

xccutivc Dircct r f, r orrcctl nal Managed Ilcal!h 'arc.

II

in erel) ,

I dd L

fitch ,11. \II D

Pr' Id III

T xas Ie h nive lIy lIealth 'cicnces 'cntcr

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 5

Section 4

Objectives, Scope, and Methodology

Objectives

The objectives of this audit were to:

Examine the shortfall reported by the Correctional Managed Health Care

Committee for fiscal year 2009, the projected shortfall reported by the

Correctional Managed Health Care Committee for the 2010-2011

biennium, and any projected shortfall reported in the Correctional

Managed Health Care Committee’s legislative appropriation request for

fiscal years 2012 and 2013.

Follow up on selected recommendations in State Auditor’s Office Report

No. 07-017 (March 2007), An Audit Report on Correctional Managed

Health Care Funding Requirements.

Scope

The scope of this audit covered Texas Tech University Health Sciences

Center’s (TTUHSC) projected and actual deficit calculations for fiscal years

2009 through 2011. Auditors also reviewed the Correctional Managed Health

Care Committee’s oversight and its projected deficits for fiscal years 2012 and

2013. (According to the Correctional Managed Health Care Committee, the

higher education institution health care providers cannot project expected

deficits for fiscal years 2012 and 2013 until they know how much the

Legislature will appropriate for their services.) In addition, auditors followed

up on a previous state auditor recommendation at TTUHSC.

Methodology

The audit methodology consisted of collecting information and

documentation, performing selected tests and other procedures, analyzing and

evaluating the results of the tests, and conducting interviews with

management and staff at TTUHSC, the Correctional Managed Health Care

Committee, and the Department of Criminal Justice.

According to the Society for Human Resource Management, fringe benefits

are benefits granted to employees in addition to their current base salary or

wages (for example, cash, merchandise, services, health insurance, pension

plans, holidays, and paid vacations).

For this audit, the State Auditor’s Office considered the following to be fringe

benefits:

Optional retirement program expenditures.

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 6

Old-age, survivors, and disability insurance expenditures.

Old age, survivors, disability, and health insurance expenditures.

Premium sharing expenditures for accidental death and dismemberment,

health, life, and vision.

The State Auditor’s Office did not include benefits such as paid leave in its

interpretation of fringe benefits.

Information collected and reviewed included the following:

Contract between the Correctional Managed Health Care Committee and

the Department of Criminal Justice, and contract between the Correctional

Managed Health Care Committee and TTUHSC.

Correctional Managed Health Care Committee and TTUHSC policies and

procedures.

Revenue TTUHSC received from the Correctional Managed Health Care

Committee.

TTUHSC’s correctional managed care expenditures related to salaries and

benefits, hospital costs, professional services, regional medical facility

contracts, and pharmacy costs.

Budgeting process documentation.

Financial reports that TTUHSC submitted to the Correctional Managed

Health Care Committee.

TTUHSC financial systems.

Procedures and tests conducted included:

Tests of expenditure data, including verification of invoices, purchase

orders, reasonableness of expenditures in the deficit calculation, and

appropriateness of amounts billed for offender health care for fiscal years

2009 and 2010.

Verification of amounts paid by the Correctional Managed Health Care

Committee and received by TTUHSC.

Review of deficit calculations for fiscal years 2009 and 2010.

Review of TTUHSC financial systems used to provide information to the

Correctional Managed Health Care Committee and to generate related

financial reports.

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 7

Interviews with management and staff at TTUHSC, the Correctional

Managed Health Care Committee, and the Department of Criminal Justice.

Analysis of employee salary actions data.

Criteria used included the following:

Texas Government Code, Chapter 501.

Title 1, Texas Administrative Code, Chapter 202.

Riders 41 and 42, page V-22, the General Appropriations Act (81st

Legislature).

Rider 61, page V-24, the General Appropriations Act (81st Legislature).

Riders 82 and 83, page V-28, the General Appropriations Act (81st

Legislature).

TTUHSC and Correctional Managed Health Care Committee policies and

procedures.

Contract between the Correctional Managed Health Care Committee and

TTUHSC.

Project Information

Audit fieldwork was conducted from May 2010 through January 2011. We

conducted this performance audit in accordance with generally accepted

government auditing standards. Those standards require that we plan and

perform the audit to obtain sufficient, appropriate evidence to provide a

reasonable basis for our findings and conclusions based on our audit

objectives. We believe that the evidence obtained provides a reasonable basis

for our findings and conclusions based on our audit objectives.

The following members of the State Auditor’s staff performed the audit:

Courtney Ambres-Wade, CGAP (Project Manager)

Ileana Barboza, MBA, CGAP, CICA (Assistant Project Manager)

Michelle Ann Feller, CIA (Assistant Project Manager)

Shahpar M. Ali, CPA, M/SBT

Jennifer D. Brantley, CPA

Ann E. Karnes, CPA

Seorin Kim, CPA

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 8

Jennifer Wiederhold, CGAP

Michael Yokie, CISA

Brian York

Charles P. Dunlap, Jr., CPA (Quality Control Reviewer)

Nicole M. Guerrero, MBA, CIA, CGAP, CICA (Audit Manager)

Attachment

An Audit Report on Correctional Managed Health Care at the Texas Tech University Health Sciences Center

SAO Report No. 11-019

February 2011

Page 9