Texas Jail Commission Audit, TX SAO, 2006

Download original document:

Document text

Document text

This text is machine-read, and may contain errors. Check the original document to verify accuracy.

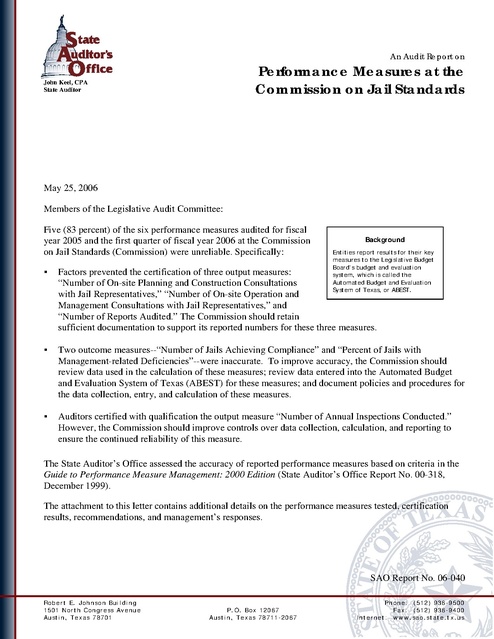

An Audit Report on Performance Measures at the Commission on Jail Standards John Keel, CPA State Auditor May 25, 2006 Members of the Legislative Audit Committee: Five (83 percent) of the six performance measures audited for fiscal year 2005 and the first quarter of fiscal year 2006 at the Commission on Jail Standards (Commission) were unreliable. Specifically: Background Entities report results for their key measures to the Legislative Budget Board’s budget and evaluation system, which is called the Automated Budget and Evaluation System of Texas, or ABEST. Factors prevented the certification of three output measures: “Number of On-site Planning and Construction Consultations with Jail Representatives,” “Number of On-site Operation and Management Consultations with Jail Representatives,” and “Number of Reports Audited.” The Commission should retain sufficient documentation to support its reported numbers for these three measures. Two outcome measures--“Number of Jails Achieving Compliance” and “Percent of Jails with Management-related Deficiencies”--were inaccurate. To improve accuracy, the Commission should review data used in the calculation of these measures; review data entered into the Automated Budget and Evaluation System of Texas (ABEST) for these measures; and document policies and procedures for the data collection, entry, and calculation of these measures. Auditors certified with qualification the output measure “Number of Annual Inspections Conducted.” However, the Commission should improve controls over data collection, calculation, and reporting to ensure the continued reliability of this measure. The State Auditor’s Office assessed the accuracy of reported performance measures based on criteria in the Guide to Performance Measure Management: 2000 Edition (State Auditor’s Office Report No. 00-318, December 1999). The attachment to this letter contains additional details on the performance measures tested, certification results, recommendations, and management’s responses. SAO Report No. 06-040 Robert E. Johnson Building 1501 North C ongre ss Avenue Austin, Te xas 78701 P.O. Box 12067 Austin, Te xas 78711-2067 Phone: (512) 936-9500 Fax : (512) 936-9400 Interne t: www.sao.state.tx .us Members of the Legislative Audit Committee May 25, 2006 Page 2 The Commission generally agrees with our recommendations, and we appreciate its cooperation during this audit. If you have any questions, please contact Verma Elliott, Audit Manager, or me at (512) 936-9500. Sincerely, John Keel, CPA State Auditor Attachment cc: Members of the Commission on Jail Standards Mr. Terry Julian, Executive Director, Commission on Jail Standards This document is not copyrighted. Readers may make additional copies of this report as needed. In addition, most State Auditor’s Office reports may be downloaded from our Web site: www.sao.state.tx.us. In compliance with the Americans with Disabilities Act, this document may also be requested in alternative formats. To do so, contact our report request line at (512) 936-9880 (Voice), (512) 936-9400 (FAX), 1-800RELAY-TX (TDD), or visit the Robert E. Johnson Building, 1501 North Congress Avenue, Suite 4.224, Austin, Texas 78701. The State Auditor’s Office is an equal opportunity employer and does not discriminate on the basis of race, color, religion, sex, national origin, age, or disability in employment or in the provision of services, programs, or activities. To report waste, fraud, or abuse in state government call the SAO Hotline: 1-800-TX-AUDIT. Attachment Performance Measure Certification Results Auditors tested the accuracy of the Commission on Jail Standards’ (Commission) key outcome performance measures for fiscal year 2005 and its key output measures for fiscal year 2005 and the first quarter of fiscal year 2006.1 Table 1 summarizes the certification results from audit testing. Table 1 Commission on Jail Standards (Agency No. 409) Fiscal Year Results Reported in ABEST A, Outcome, Number of Jails Achieving Compliance 2005 211 Inaccurate A, Outcome, Percent of Jails with Management-related Deficiencies 2005 15% Inaccurate 2005 252 2006 (1st Quarter) 69 2005 73 2006 (1st Quarter) 4 2005 171 2006 (1st Quarter) 41 2005 6,248 2006 (1st Quarter) 1,593 Related Objective or Strategy, Classification, and Description of Measure A.1.1, Output, Number of Annual Inspections Conducted A.2.1, Output, Number of On-site Planning and Construction Consultations with Jail Representatives A.2.2, Output, Number of On-site Operation and Management Consultations with Jail Representatives A.3.1, Output, Number of Reports Audited a a Certification Results Certified with Qualification Factors Prevent Certification Factors Prevent Certification Factors Prevent Certification In fiscal year 2006, the name of this measure was changed to “Number of Reports Analyzed.” A measure is Certified if reported performance is within +/-5 percent of actual performance and if controls appear adequate to ensure accuracy for collecting and reporting performance data. A measure is Certified With Qualification if reported performance is within +/-5 percent of actual performance but controls over data collection and reporting are not adequate to ensure continued accuracy. A measure is Inaccurate when reported performance is not within +/-5 percent of actual performance or there are more than two errors in the sample tested. Factors Prevent Certification when actual performance cannot be determined because of insufficient documentation and inadequate controls or when there is deviation from the measure definition and the auditor cannot determine the correct result. 1 Outcome measures are reported only annually; output measures are reported quarterly. Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 1 The Commission Should Improve its Reviews of and Policies and Procedures for Reporting Performance Measures For all performance measures tested, the Commission does not have sufficient controls to ensure its reported performance measures are accurate. Specifically: The Commission does not perform supervisory review of performance measure calculations. The Commission does not review data that has been entered into the Automated Budget and Evaluation System of Texas (ABEST) before it is released into ABEST. The Commission does not have written policies and procedures documenting data collection, entry, calculation, and review of performance measures. Lack of supervisory review and policies and procedures impairs the accuracy of reported performance measures. Recommendations The Commission should: Implement a supervisory review process to ensure that the data entry, calculation, and reporting to ABEST of performance measure results are accurate. Develop and implement written policies and procedures for data entry, calculation, and reporting of performance measures. Management’s Responses Commission staff have developed a documented review and verification of performance measure calculations and ABEST data entry (prior to release), and are in the process of developing written policies and procedures regarding these activities. These policies and procedures will include clear and concise instructions on exactly how each measure is calculated, including formulas, documented data sources, and location of all data sources. Documented review processes have been implemented and will be included in the policy and procedures revisions. Definitions have been clarified in the ABEST descriptions of relevant performance measures; staff is awaiting responses/approval by the LBB and the Governor’s Office on Budget and Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 2 Policy. Retention periods of less than three (3) years for any documentation employed in performance measure calculations has been extended to three (3) years. Key Measures Number of On-site Planning and Construction Consultations with Jail Representatives Number of On-site Operation and Management Consultations with Jail Representatives Factors prevented the certification of these measures because the Commission did not maintain adequate documentation to support the results it reported in ABEST. The Commission has little documentation to support the number of on-site consultations reported in ABEST, and documentation that does exist may not indicate which type of consultation (planning and construction or operation and management) took place or what was discussed during the consultation. Therefore, the number of consultations reported in ABEST could not be re-created. Results: Factors Prevent Certification Actual performance cannot be determined because of insufficient documentation and inadequate controls or when there is deviation from the measure definition and the auditor cannot determine the correct result. Recommendations The Commission should: Develop and maintain all source documentation that supports the performance measure results, including a synopsis of each on-site consultation. Develop written policies and procedures for performing on-site planning and construction and operation and management consultations with jail representatives. Management’s Responses New documentation has been developed as additional data support for the tracking of on-site consultations to ensure accurate reporting of these planning and construction and management consultations. Policies and procedures are being revised to incorporate the new documentation into the clear and concise instructions for the process of documenting and reporting these measures. Definitions have also been clarified. Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 3 Number of Reports Audited Results: Factors Prevent Certification Actual performance cannot be determined because of insufficient documentation and inadequate controls or when there is deviation from the measure definition and the auditor cannot determine the correct result. Factors prevented the certification of this measure because the Commission did not maintain adequate documentation to support the number of reports received, analyzed, or revised. Therefore, the number of reports audited as reported in ABEST could not be re-created. Specifically: The Commission does not consistently date-stamp original reports upon receipt. The Commission overwrites electronic checklists indicating reports received, and it does not maintain hard copies. The Commission includes reports that have been revised in this measure. It disposes of a handwritten checklist indicating monthly revised reports after one year. Recommendation The Commission should date-stamp all reports received and maintain source documentation to support the performance measure results. Management’s Responses Staff has been instructed to ensure consistent procedures in date-stamping original reports as they are received. Electronic checklists are being stored, rather than over-written, and hard copies of these checklists will be produced and retained. The hard copies of the checklists, as well as both original and revised reports, will be retained for a minimum of three (3) years. Policies and procedures are being revised to reflect these changes. Number of Jails Achieving Compliance This measure was inaccurate because testing found that the number of jails achieving compliance was incorrect in 5.2 percent of the items Results: Inaccurate tested. For example, the Commission included two counties as Reported performance is not within +/-5 percent compliant that had not received an inspection within the fiscal of actual performance or year, and it excluded two counties that had received compliant there are more than two errors in the sample inspections. Jails are certified when they receive a compliant tested. rating on their most recent inspection. The measure definition also does not contain enough information to be clearly understood and easily recalculated. The measure definition is not specific Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 4 regarding what constitutes a recent inspection or which inspections are to be counted. Recommendations The Commission should: Work with the Legislative Budget Board to improve the performance measure calculation and methodology. Ensure that data is uniformly and consistently calculated and reported within that definition and methodology. Management’s Responses Revisions of the definition, data source and methodology have been submitted to the LBB and Governor’s Office for approval, to clarify and expand the information, in order to ensure understanding and proper calculation of this measure. These clarifications are more specific in terms of which inspections, and therefore which compliant jails, are to be counted. These steps will ensure that performance measure data is uniformly and consistently calculated and reported, and that the calculations and numbers reported are consistent with the definitions and methodology. Percentage of Jails with Management-related Deficiencies This measure was inaccurate because auditors identified an 11.67 percent variance between the recalculated performance measure and the Results: Inaccurate measure the Commission reported in ABEST. This measure is Reported performance is not within +/-5 percent calculated by dividing the number of non-compliant jails with of actual performance or management deficiencies by the total number of operational jails. there are more than two errors in the sample tested. In addition, audit testing found that the number of jails with management-related deficiencies was incorrect for 5.2 percent of the items tested. For example, the Commission included a jail that was actually compliant, and it included three counties whose deficiencies were not clearly management-related. The Commission uses a checklist to determine what types of deficiencies are management-related, but that checklist is subject to interpretation and is not always adhered to. The measure definition also does not contain enough information to be clearly understood and easily recalculated. There are discrepancies within the definition and many of the terms in the definition are not defined: Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 5 There were inconsistencies among the measure name, definition, and methodology. The measure definition includes “operational standards” and “management deficiencies,” while the name and methodology include only “management deficiencies.” It is not clear which jails should be included as “operational jails.” Recommendation The Commission should work with the Legislative Budget Board to improve the performance measure calculation, methodology, and definition; ensure that data is uniformly and consistently calculated and reported within that definition and methodology; and document the types of deficiencies that are to be included in the measure. Management’s Responses Revisions that clarify the definition, data source, and methodology of this measure have been submitted to the LBB and Governor’s Office for approval. These revisions reflect new procedures to ensure uniform and consistent calculation and reporting of this information. Policies and procedures are also being revised to incorporate the new definitions and will include specific steps in recording, calculating and reporting of jails found to be noncompliant due to deficiencies that may be remedied through adjustment(s) to internal jail procedures by jail management staff. Number of Annual Inspections Conducted The Commission’s reported result for this measure was accurate. However, this measure was certified with qualification because the Results: Certified With Qualification Commission does not review calculations before they are Reported performance is within +/- 5 entered and released into ABEST and does not have written percent of actual performance, but policies and procedures for entering data, calculating results, controls over data collection and reporting are not adequate to ensure and reporting performance measure results into ABEST. To continued accuracy. improve accuracy, the Commission needs to implement the recommendations on page 2. Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 6 Management’s Responses Commission staff has implemented a documented review process for the calculation and reporting of this measure. Revisions to the definition, data limitations, data source, and methodology have been submitted to the LBB and the Governor’s Office for approval. Policies and procedures revisions are being developed consistent with the foregoing in order to ensure accurate, uniform and consistent calculation and reporting of this data. Specific Information Technology Controls Should Be Improved General controls over the Commission’s network and databases appear adequate to ensure that the data supporting the Commission’s reported performance measures is accurate and reliable. Auditors did not test application controls because the Commission uses only Microsoft products (such as Access and Excel) and does not use other automated applications. Auditors also identified weaknesses related to physical security and business continuity. These weaknesses put the Commission at risk of network failure or loss of data. Specifically: The Commission’s full network back-up tapes, which contain sensitive accounting and human resources information, are stored at an unsecured location. Only one individual has administrator rights to access the network. Title 1, Texas Administrative Code, Section 202.20, requires the continuity of information resources in the event of a business disruption. The server is not located in a temperature-controlled room. In addition, physical access to the server room is not adequately monitored. The Commission has an inspection database, but it does not use this database to calculate performance measure results. The Commission does not test its disaster recovery plan at least annually as required by the Title 1, Texas Administrative Code, Section 202.24 (5). Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 7 Recommendations The Commission should: Store its full back-up tapes in a secure location. Give administrator access to an additional employee who can serve as a backup for information technology support. Identify options to control the heat in the server room and control access to that room. Expand the functionality of the inspection database so that it can be used to calculate performance measure results. Test its disaster recovery plan at least annually to ensure it is current. Management’s Responses Weaknesses related to physical security and business continuity, identified by the State Auditors, are being addressed by Commission staff in order to reduce, if not eliminate, the risk of network failure or loss of data. The full back-up tapes are being stored in a secure location. Passwords for administrator access are kept in a locked cabinet in the Agency suite. An employee selected by the Executive Director or the Deputy Director will be provided with these codes should backup access by someone other than the current administrator be required. The temperature in the server room has been a concern for quite some time, and the staff has investigated options for a system to control the heat. Due to the Agency’s limited appropriation, however, such an expenditure is not a viable option. Whenever current budget constraints are no longer an issue, the staff will arrange to have a temperature control system installed. The server room is kept locked, and the IT staff member has one key; another key is kept in a locked key-box, which may be accessed by the Deputy Director and two additional staff members. Expanding the data and formulas available for the inspection database has been a topic of discussion among Agency staff; the development of the database into a useful tool for calculating performance measure results, as well as for gathering and utilizing other information regarding the jails under Commission authority, are but one of the long-term goals identified by the Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 8 staff. The Agency is currently, however, unable to budget the cost of bringing in temporary or even permanent staff in order to develop such a program. Again, when the current budget restrictions are eased, this will be an item that will certainly be revisited. Commission staff is developing policies and procedures, to include annual review of the disaster recovery plan to ensure these plans are currently viable. Staff is also working to coordinate with DIR to ensure a current disaster recovery plan for information technology. Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 9 Objectives, Scope, and Methodology Objectives The audit objectives were to determine whether the Commission (1) is accurately reporting its performance measures to ABEST and (2) has adequate control systems in place over the collection and reporting of its performance measures. Scope The audit scope covered key performance measure results reported by the Commission for fiscal year 2005 and the first quarter of fiscal year 2006. Auditors also reviewed controls over the submission of data used in reporting performance measures and traced performance measure information to the original source documents when possible. Methodology The audit methodology included selecting measures to audit, auditing results for accuracy and adherence to the measure definitions, evaluating controls over the performance measure certification process and related information systems, and testing samples of source documentation when possible. Project Information Auditors conducted fieldwork from March through April 2006. This audit was conducted in compliance with generally accepted government auditing standards. The following staff of the State Auditor’s Office performed the audit: Jennifer Wiederhold (Project Manager) Lauren L. Godfrey Jennifer Lehman, MBA Kelly Vogler Mary Ann Wise, CPA J. Scott Killingsworth, CIA, CGFM (Quality Control Reviewer) Charles P. Dunlap, Jr., CPA (Quality Control Reviewer) Verma Elliott, MBA, CGAP (Audit Manager) Attachment An Audit Report on Performance Measures at the Commission on Jail Standards SAO Report No. 06-040 May 2006 Page 10